Reintroducing the Vivad Se Vishwas Scheme in Union Budget 2024

Home > Reintroducing the Vivad Se Vishwas Scheme in Union Budget 2024

August 22, 2024

Introducing Vivad Se Vishwas Scheme, 2024

Executive Summary

Key Features of the Direct Tax Vivad Se Vishwas Scheme ( DT VSVS), 2024

Scheme Overview:

- The Direct Tax Vivad Se Vishwas Scheme, 2024 (DT VSVS 2024 Scheme) is introduced in the Finance (No. 2) Bill, 2024 as part of Union Budget 2024, announced on July 23, 2024

- The scheme draws applicability, procedure, and settlement methods from the Direct Tax Vivad Se Vishwas Act, 2020 (DT VSVS 2020 Scheme)

- The start date and sunset date for the scheme are yet to be notified

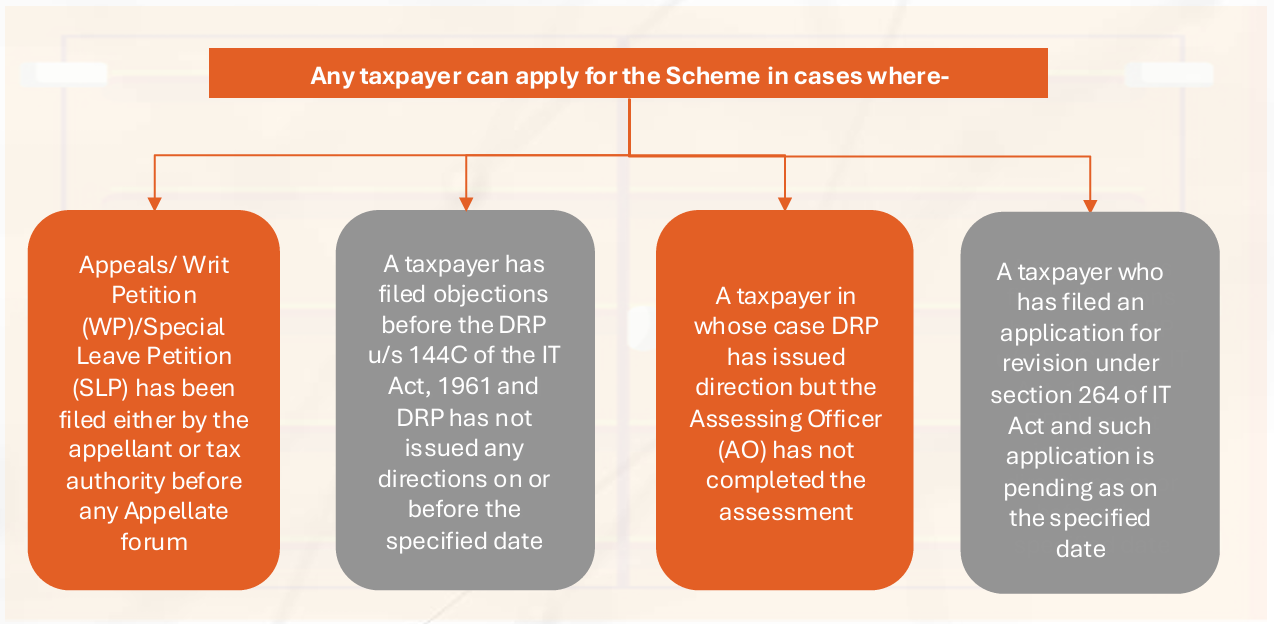

Eligibility for settlement:

Disputes/appeals, including writs and special leave petitions [Appeal(s)], whether filed by the taxpayer or the tax authorities and are pending as on 22 July 2024 before the following forums:

- The Supreme Court, High Court, Income Tax Appellate Tribunal (ITAT), Commissioner/Joint Commissioner (Appeals) [CIT(A)]

- The Dispute Resolution Panel (DRP) or where DRP directions have been issued but the final assessment order is awaited

- Revision petitions pending before the Commissioner of Income Tax

Settlement Process:

To resolve eligible disputes, taxpayers must pay amounts determined by the Designated Authority (DA) under the 2024 Scheme and follow the procedure prescribed

” For the resolution of certain income tax disputes pending in appeal, I am also proposing the Vivad Se Vishwas Scheme, 2024. I hope that taxpayers will make use of this opportunity to get relief from the vexatious litigation process” – Hon’ble Finance Minister, India“

Background

Given the success of the previous DTVSVS 2020 scheme and the growing backlog of litigation at various

appellate levels, Hon’ble Finance Minister, 2024 reintroduced Vivad Se Vishwas Scheme, 2024 (2024

Scheme).

Triumph of VSVS 2020

- As of 4 July 2024

• No. of pending income tax litigations where settlement sought by the declarants – 1,31,714

• Number settled finally out of above declarations sought – 1,13,894

• Payments made against Disputed Tax – INR 75,788.25 Cr - Remarkable progress has facilitated the payment of INR 75,788.25 crore(s) as taxes showcasing the scheme’s effectiveness in streamlining tax disputes and fostering a more efficient tax resolution process

- VSVS 2.0 stands as a testament to the government’s commitment to simplifying tax compliance and dispute resolution, offering a major boost to the nation’s financial system

Key Terms of the DTVSVS 2024 Scheme

The Finance Act, 2024 has inserted a new Chapter IV to provide the DTVSVS 2024 Scheme.

| Term | Definition |

|---|---|

|

Appellate forum |

Includes the Supreme Court, High Court, ITAT, CIT(A), or Joint CIT(A), as

applicable. |

|

Declarant |

A person who files a declaration. |

|

Declaration |

The declaration filed by the taxpayer under the Scheme. |

|

Designated

authority |

An officer not below the rank of a Commissioner of Income-tax notified by the Principal Chief Commissioner for the purposes of the Scheme. |

|

Disputed fee |

Fee determined under the Income-tax Act for which an appeal has been filed. |

|

Disputed income |

Whole or so much Income as is relatable to the disputed tax. |

|

Disputed interest |

Interest determined under the Income-tax Act where it is not charged on disputed

tax and an appeal has been filed. |

|

Disputed penalty |

Penalty determined under the Income-tax Act where it is not levied on disputed

income or tax and an appeal has been filed. |

|

Disputed tax |

Income-tax payable by the appellant, including surcharge and cess, based on the potential outcome of various appeals, objections, or revisions. |

|

Last date |

Date notified by the Central Government in the Official Gazette. |

|

Tax arrear |

Includes disputed tax, interest chargeable or charged on such disputed tax, penalty leviable or levied on disputed tax, or disputed interest or disputed penalty or disputed fee (or any combination thereof related to the disputed tax) |

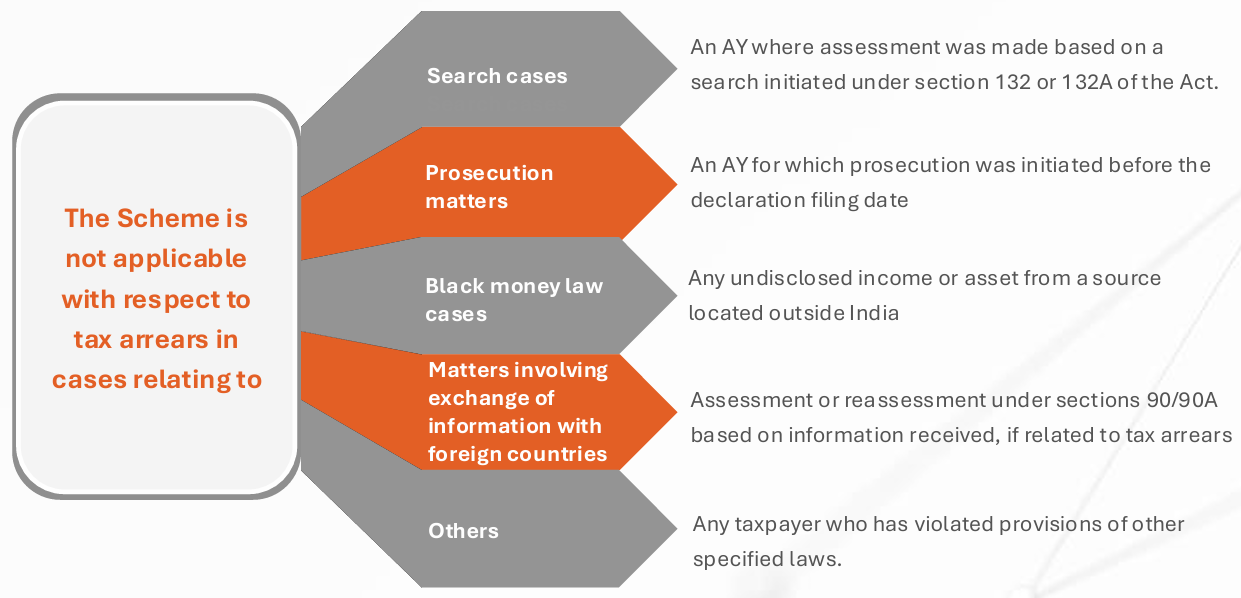

Eligibility Criteria for Taxpayers

Ineligibility Criteria & Dispute Settlement

Guidelines

Settlement Amount for Dispute

For cases with disputed tax, interest charged or chargeable and penalty levied or leviable

| Nature of Dispute/ Tax Arrear | Settlement before 31 December 2024 | Settlement on or after the 01 January 2025 but on or before last date to be notified |

|---|---|---|

|

The declarant was an appellant at the same

appellate forum on or before January 31, 2020. |

110% of the disputed tax |

120% of the disputed tax |

|

The declarant is an appellant from February 1, 2020, up to the specified date. |

100% of the disputed tax |

110% of the disputed tax |

For cases with disputed interest or disputed penalty or disputed fee

| Nature of Dispute/ Tax Arrear | Settlement before 31 December 2024 | Settlement on or after the 01 January 2025 but on or before last date to be notified |

|---|---|---|

|

The declarant was an appellant at the same appellate forum on or before January 31, 2020. |

30% of disputed interest/

penalty/fee |

35% of disputed

interest/penalty/fee |

|

The declarant is an appellant from February 1, 2020, up to the specified date. |

25% of disputed interest/

penalty/fee |

30% of disputed

interest/penalty/fee |

*Settlement amounts payable to be reduced to 50% in following cases:-Where appeal/writ/Special leave petition is filed by the tax authorities.-The Appellant’s case is favorably covered by the ITAT/High Court decision in taxpayer’s own case.

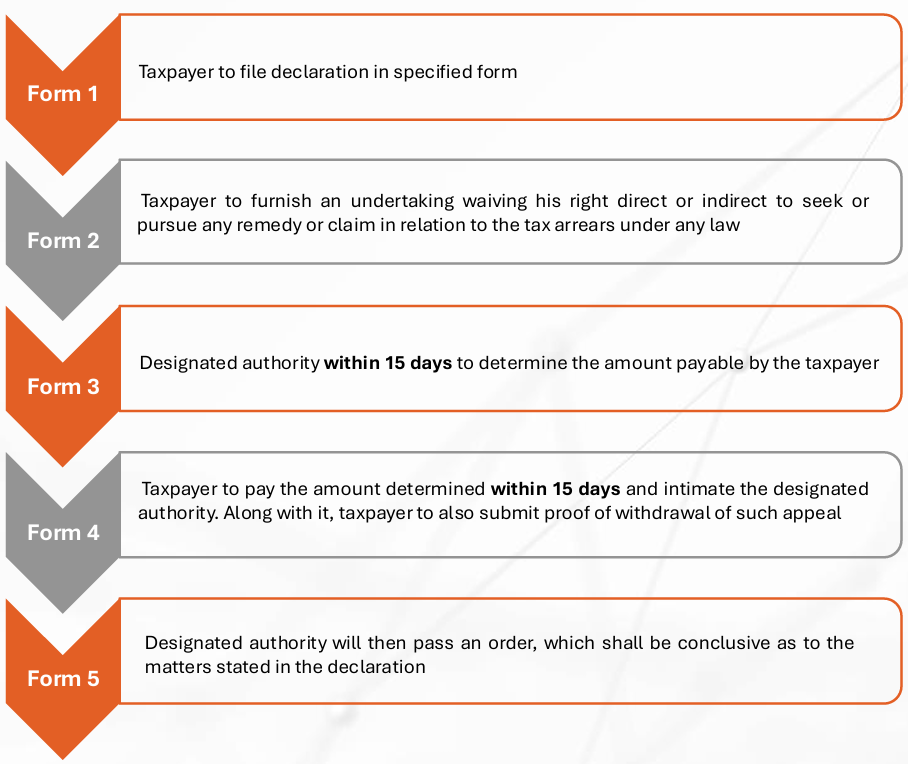

Procedural Requirements for Relief

Any Assessee opting for the scheme shall follow the following procedure as specified in the guidelines

• The above forms are further discussed in the ensuing slides. The above forms are based on the DTVSVS 2020 Scheme and the Forms for DTVSVS 2024 scheme are yet to be notified. However, given the similarity in the schemes, there may be minor changes in the fields and format of the Form while the essence remaining intact

Important: The declaration under the Scheme shall be deemed not to have been made if,–

(a) any material particular furnished is found to be false at any stage; or

(b) Violation of conditions of the Scheme; or

(c) the declarant acts in any manner which is not in accordance with the undertaking given by him.

All the proceedings and claims which were withdrawn under this section and all the consequences under the Income-tax Act against the declarant shall be deemed to have been revived.

Form Details & Immunities

An in-depth understanding of the forms specified earlier is detailed below:

| Form No. | Form For | Form Content |

|---|---|---|

|

Form 1 |

Declaration |

Form 1 has 5 sections: Part A: General information and eligibility details Part B: Dispute-related information Part C: Tax arrears details Part D: Amount payable details Part E: Payments made against tax arrears Part F: Net amount payable or refundable to the appellant |

|

Form 2 |

Undertaking |

This form pertains to the undertaking in which the taxpayer waives all rights to

any remedy or claim related to the matter they choose to settle under the DT

VSVS Scheme. |

|

Form 3 |

Granting of

Certificate |

The designated authority will issue an electronic certificate detailing the tax

arrears and amount due. The declarant must pay the amount specified in

Form 3 within the given timeframe, or the Form 1 declaration will be void. |

|

Form 4 |

Intimation of

payment and

proof of

Withdrawal |

Payment details per Form 3 must be submitted to the designated authority

using this form, along with proof of withdrawal of any related appeals,

petitions, or claims filed by the declarant. |

|

Form 5 |

Issuance of order |

The designated authority will issue an order in this form, confirming that the

taxpayer has paid the dues stated in Form 3 and granting immunity from

prosecution or penalty proceedings. |

Immunity & Essential Considerations

- Any amount paid under a declaration made is non-refundable.

- If the declarant paid more than the amount due before filing the declaration, they are entitled to a refund of the

excess but without interest under section 244A of the Income-tax Act. - Except as specifically stated, the scheme grants no additional benefits, concessions, or immunity beyond the

matters covered in the declaration. - The order issued by the designated authority is final and cannot be reopened in any other proceedings.

- No new proceedings for offences, penalties, or interest can be initiated.

- Appellate forums, arbitrators, conciliators, or mediators cannot rule on cases where the designated authority has

issued an order. - Settling the dispute does not set a precedent for conceding a tax position i.e., the tax authority cannot

proceed for any other AY or proceeding based on declaration or settlement under the DTVSVS Scheme.

How can SBC assist you?

SBC Comments:

The proposed scheme is advantageous for taxpayers who have been experiencing lengthy litigation cycles or anticipate high litigation costs:

✓ Settlements do not set precedents, preserving case uniqueness.

✓ Encourages cooperation between taxpayers and authorities.

✓ Provides clear resolution and certainty on tax obligations.

✓ Helps avoid lengthy and costly litigation.

✓ Waives interest and penalties, reducing financial strain.

✓ Allows use of available tax losses, enhancing financial stability.

✓ It significantly reduces the costs associated with legal disputes

However, the following issues may arise, and it is advisable to seek professional guidance to address them

✓Immediate cash outflows may disrupt budgeted expenses.

✓Quick decisions and fast analysis are required due to tight deadlines.

✓Partial settlement is not allowed; all issues must be resolved or litigated.

✓The scheme doesn’t address double taxation or high-stakes cases; APA or MAP may be needed

✓There were FAQs issued even for application of the earlier DTVSVS Scheme and it shall be necessary to see the tax positions on calculating disputed tax or arrears for settlement.

SBC Support:

Navigating the Vivad se Vishwas Scheme 2.0 can be complex, and our team at SBC is here to support you

every step of the way. Here’s how we can assist:

- Eligibility Assessment: We’ll review your litigation status to determine scheme qualification and offer tailored advice.

- Documentation & Filing: Our experts will assist in gathering and preparing required documents for timely and accurate submission under VSVS 2.0.

- Compliance & Risk Management: We’ll guide you through compliance, identify risks, and develop mitigation strategies.

- Representation & Negotiation: We’ll represent and negotiate on your behalf with authorities for optimal outcomes.

SBC has extensive and exclusive experience in assisting non-resident taxpayers, including successfully filing applications under the DTVSVS 2020 Scheme. In a notable case, SBC facilitated the admission of an application that was initially rejected, by filing a WRIT Petition, ultimately securing a favorable outcome for the client.

Verify Email

Verify your email address below to download the PDF