- Hitech City, Hyderabad

- Office Hours: 10:30 am - 7:30 pm

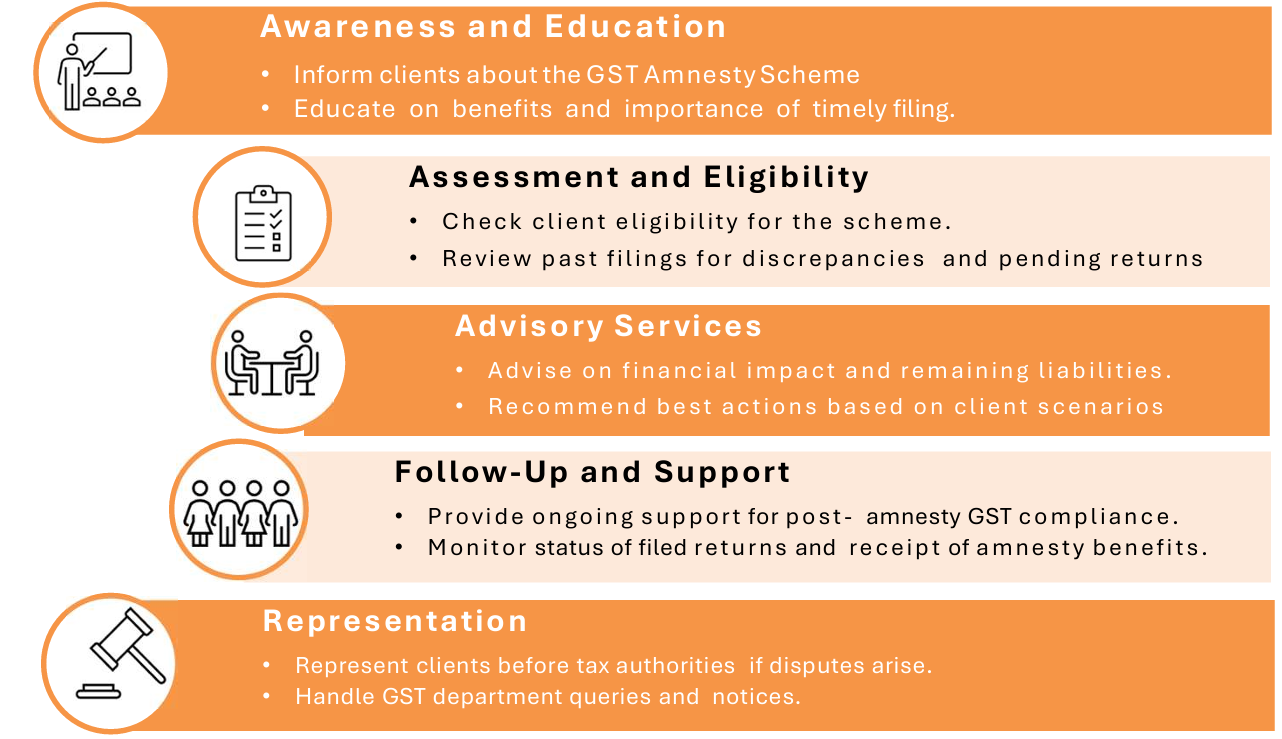

Previously (as examples shown below) are amnesty schemes under the CBIC which have typically addressed issues related to the late submission of GST monthly and Annual Returns. These initiatives aimed to alleviate penalties and encourage compliance among taxpayers. Similarly, The latest scheme, discussed in the 53rd GST Council meeting and

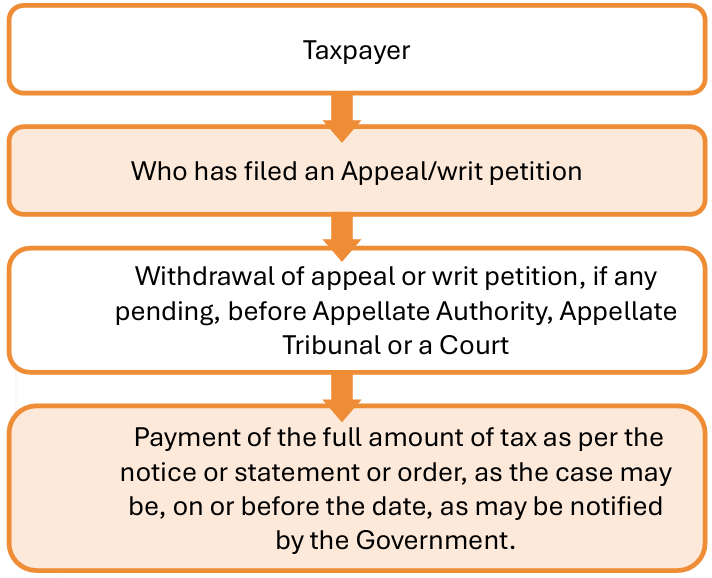

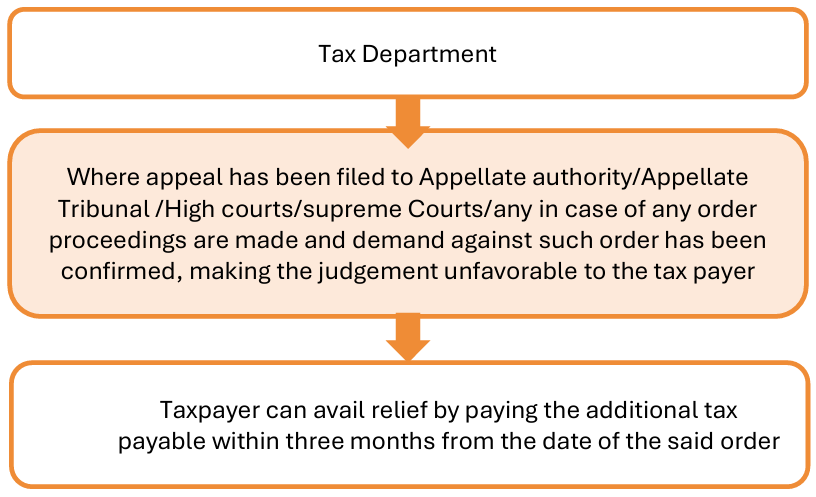

detailed in the financial bill, 2024, introduces Section 128A in CGST Act to provide conditional waiver of interest or penalty or both relating to demands raised under section 73 years 2017-18, 2018-19 and 2019-20 , in cases where demand notices have been issued under section 73and full taxliability is paid by the taxpayer before a date to be notified.

Scope: Applies specifically to demands under Section 73, which generally deals with non-fraudulent tax discrepancies and refunds.

Time Frame: Relief applicable for tax periods from FY2017-18 to FY2019-20.

Due Date for Payment: All taxes must be paid on or before March 31, 2025 as per the 53rd GST Council meeting. However, currently the law remains silent and an official notification from the government is yet to be issued.

Relief: Complete waiver of interest and penalty.

While the proposed GST Amnesty Scheme under Section 128A offers significant relief to taxpayers, it is important to understand that certain cases are noteligible for this scheme. This exclusion aims to maintain the integrity of the tax system and ensure that the scheme benefits those who comply with the law in good faith. The following are the key

exclusions:

The applicability extends to:

ii. Issued right afterward if there is a need to formally demand the payment of the tax assessed in ASMT

10.)

A. Acceptance of all allegations – Pay the demanded tax amount and avail benefits of section 128A i.e– waiver of interest and penalty.

B. Acceptance of some of the allegations – Pay tax, interest and penalties attracted towards accepted allegations.

C. Declination of all the allegations – Go for further proceedings or pay the pre-deposit for further appeals.