- Hitech City, Hyderabad

- Office Hours: 10:30 am - 7:30 pm

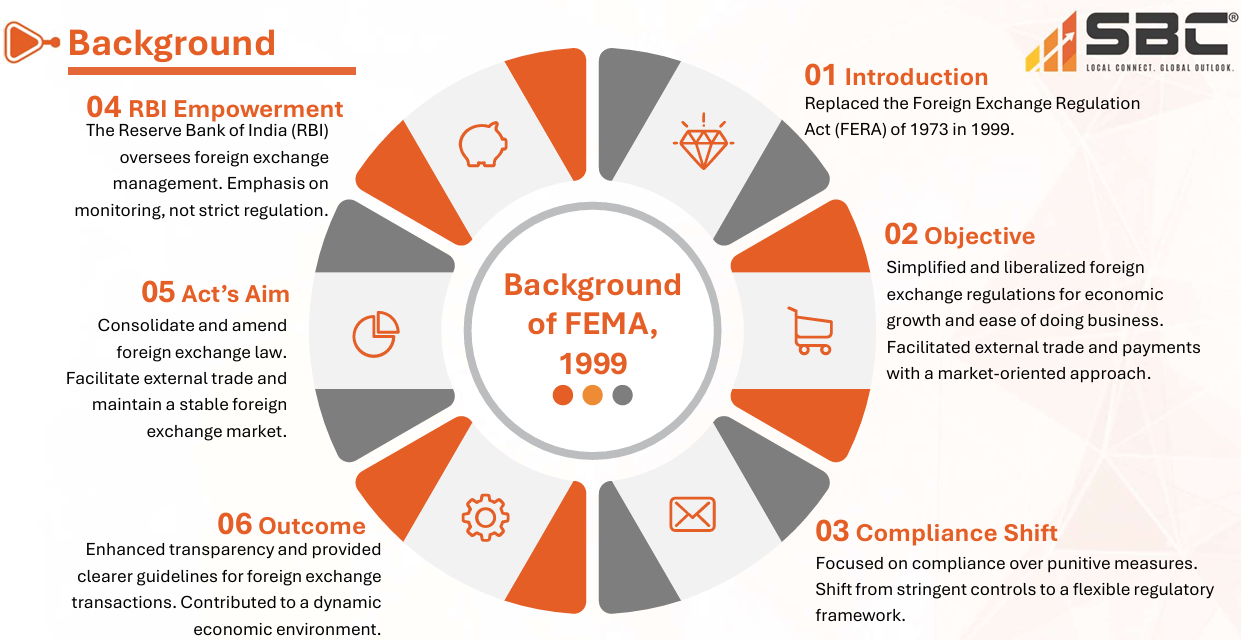

The Foreign Exchange Management Act (FEMA) of 1999 is the primary legislation governing foreign exchange transactions in India, ensuring adherence to international financial regulations. When violations occur, they can lead to penalties or legal actions. However, FEMA permits the compounding of offences, allowing offenders to pay a fee to resolve the violation without facing more severe penalties or prosecution.

The newly introduced Foreign Exchange (Compounding Proceedings) Rules, 2024, update the previous 2000 rules, aiming to streamline the process and improve transparency in handling foreign exchange violations

The new rules specify that compounding authorities will be from both the Directorate of Enforcement and the Reserve Bank of India (RBI), depending on the type of violation.

1. Director of Enforcement: Acts as the principal authority for compounding violations under Section 3(a) of FEMA, which generally deals with the illegal transfer of foreign exchange and foreign security violations.

2. RBI Officers: RBI officers of various ranks have the authority to compound other contraventions based on the amount involved in the violation:

• Violations under Rs. 60 lakhs: Assistant General Manager or higher.

• Violations under Rs. 2.5 crores: Deputy General Manager or higher.

• Violations under Rs. 5 crores: General Manager or higher.

• Violations above Rs. 5 crores: Chief General Manager or higher.

Users can not only present the presentation on the projector or computer, but they can also print out the presentation.

The applicant must submit a compounding application in the prescribed form (detailed in the annexure) to the relevant authority (RBI or Enforcement Directorate), along with a fee of Rs. 10,000 plus applicable Goods and Services Tax (GST).

The payment can be made via Demand Draft, NEFT, RTGS, or other electronic modes.

The authority may call for additional information, records, or documents relevant to the case. The applicant may be asked

to furnish further details regarding the transaction involved in the contravention.

The authority must pass the compounding order within 180 days of receiving the application, ensuring that the case is resolved quickly. The order will include the specific provisions of FEMA violated, details of the contravention, and the amount payable for compounding the offence.

Once the order is passed, the applicant must pay the compounded sum within 15 days. Failure to make the payment within the stipulated time would mean the application for compounding is void, and the violation would be dealt with as a regular contravention under FEMA.

If a contravention is compounded before adjudication, any ongoing or pending inquiry related to the violation will be discontinued. Once the compounded sum is paid, the contravention is fully settled, and no further penalties will be imposed.

A copy of the order is provided to the applicant and the Adjudicating Authority (if involved) to ensure transparency in the

process.

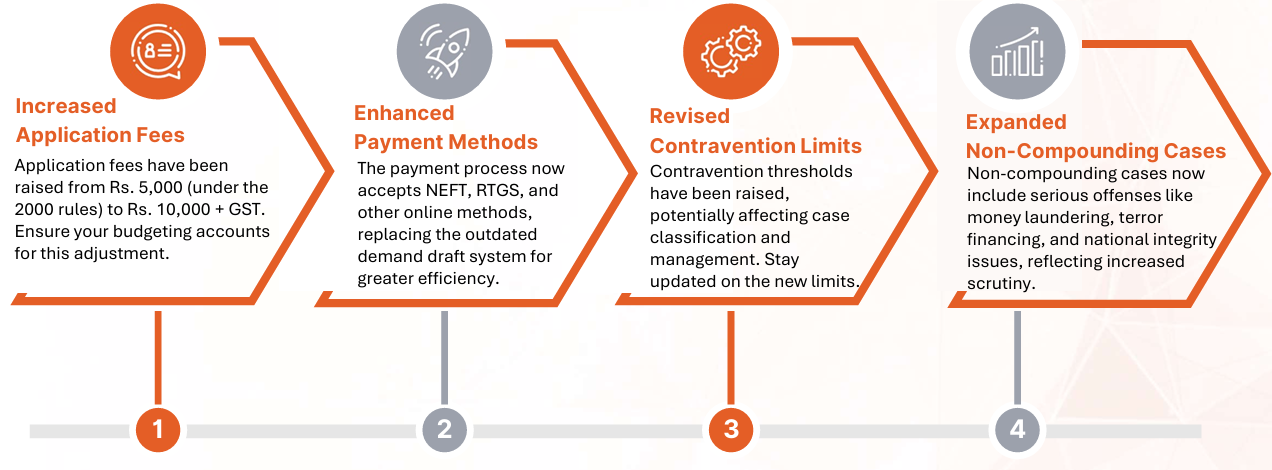

•The application fee has been raised from Rs. 5,000 (as per the 2000 rules) to Rs. 10,000 plus GST.

•Payments can now be made via NEFT, RTGS, and other online methods, moving away from the former demand draft-only requirement

Not all FEMA violations are eligible for compounding. The rules specify the following conditions where compounding is not allowed:

If the compounded sum is not paid within the specified 15-day period, the application will be nullified and considered as if no compounding application had been submitted. In such situations, the standard provisions of FEMA will take effect, potentially resulting in higher penalties or legal action.

Overview of the Indian Safe Harbour Regime

Eligible Assessee

A person who has validly opted for safe harbour rules under Rule 10TE of the Income Tax Rules, 1962.

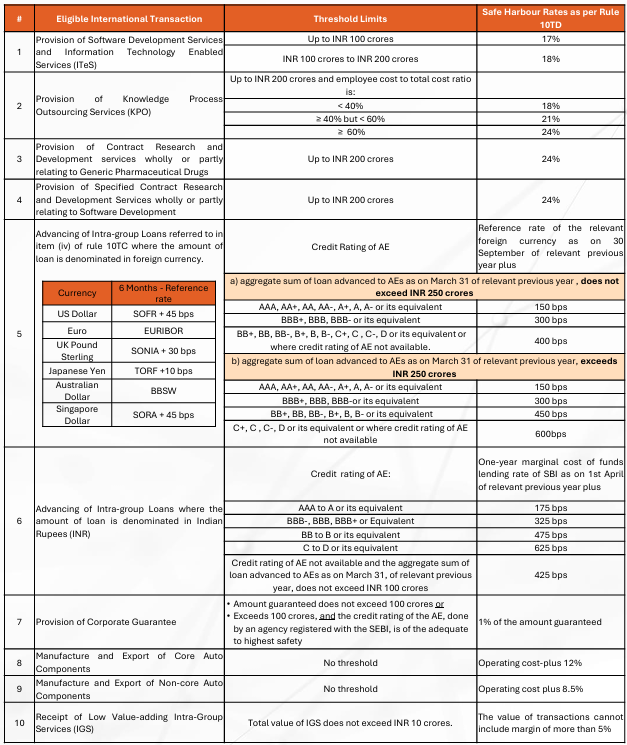

Eligible Transactions

These eligible transactions qualify for safe harbour treatment under Rule 10TB, providing a simplified and predictable transfer pricing framework.

Advantages of Choosing the Safe Harbour Approach

Enhanced Certainty

By providing advance insight into the acceptable range of profits or prices that meet Safe Harbour criteria, transactions gain a heightened level of certainty, offering stakeholders a clearer financial landscape.

Conflict Mitigation

Safe Harbour serves as an effective dispute avoidance mechanism, significantly curbing the potential for conflicts between taxpayers and revenue authorities. This fosters a more harmonious business environment, particularly significant given the high incidence of Indian Transfer Pricing litigation.

Streamlined Approvals & Assessment

Safe Harbour Rules offer a structured mechanism for application and approvals procedures, facilitating a smoother and time-bound process. This stands in stark contrast to the prolonged timelines associated with Domestic Litigation or Advance Pricing Agreements (APAs).

Comparative Compliance

In contrast to the complexities involved in Advance Pricing Agreements (APAs) and the Domestic Transfer Pricing Litigation Route, Safe Harbour Rules present a more favorable choice in terms of TP/ALP rates/margins, timelines, and associated costs. This streamlined approach can alleviate compliance burdens.

Resource Efficiency

The adoption of Safe Harbour Rules translates into substantial savings in terms of time, costs, and efforts, especially in potential litigation scenarios. This strategic choice can lead to optimized resource allocation and more efficient business operations.

Stakeholder Confidence

Safe Harbour instills confidence in taxpayers through its predictable framework, enhancing investor confidence and fostering robust business growth.

Safeguarding Reputational Capital

Choosing the Safe Harbour route mitigates the risk of reputational damage that could arise from contentious transfer pricing disputes. A clean record in compliance can enhance a company’s standing within its Group and among stakeholders.

Incentive for Voluntary Compliance

The transparent and predictable nature of Safe Harbour can incentivize voluntary compliance, enabling companies to proactively meet their transfer pricing obligations and contribute positively to the overall tax ecosystem.

Safe Harbour Rules in India: Key Points for Taxpayers

For those seeking to opt for safe harbour rules and who have undertaken in eligible international transactions, adherence to specific guidelines is imperative. Here’s a concise breakdown of the crucial aspects:

Filing Requirement

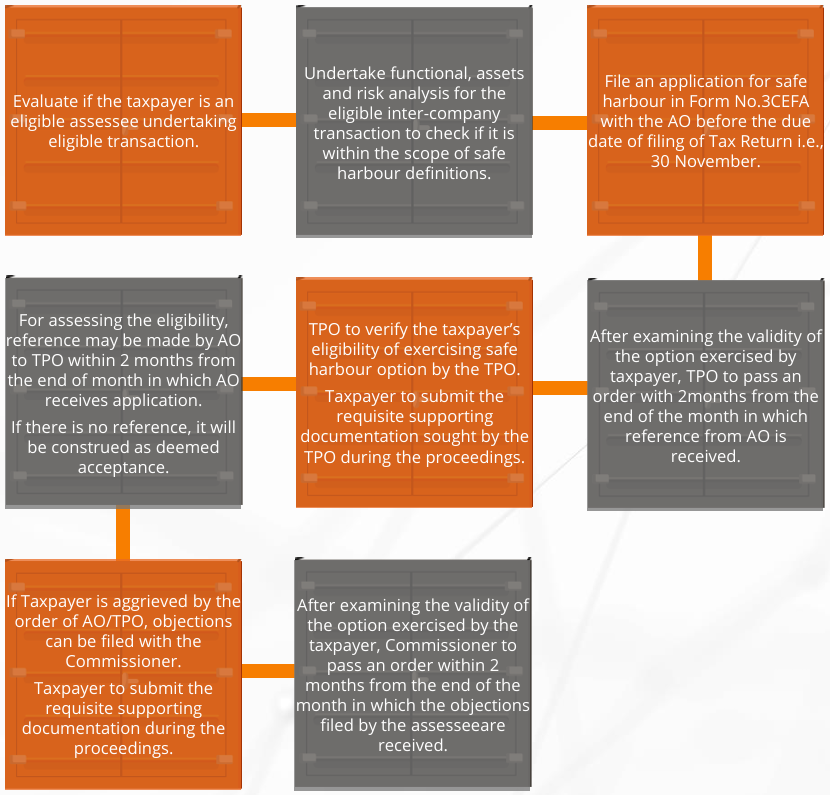

Taxpayers opting for safe harbour need to file an income return and safe harbour application (Form No 3CEFA) to the Assessing Officer, both before the stipulated deadline i.e., 30 November following the relevant FY.

Compliance Commitment

Even if opting for safe harbour, taxpayers must fulfill the prescribed transfer pricing documentation and maintain/Form 3CEB filing compliances (Rule 10TD(5) of the Rules).

Geographical Limitations

Safe harbour doesn’t apply to transactions with Associated Enterprises/Related Parties location in low or no tax countries.

Mutual Agreement Procedure (MAP)

If approved, the transfer price by the tax authorities for an eligible international transaction bars the assessee from invoking the Mutual Agreement Procedure in a double taxation avoidance agreement with a foreign entity.

Adjustment Constraints

When opting for safe harbour, comparability adjustments and prescribed variation/range benefits (tolerance band) aren’t accessible (Rule 10TD(4) of the Rules).

Duration of Choice

The option exercised remains in effect for a period as notified by the CBDT.

Transaction Scope

Safe harbour applies solely to specified transactions, while TP scrutiny exposure remains open to other transactions not eligible under safe harbour.

Deemed Acceptance

If the Assessing Officer, Transfer Pricing Officer, or the Commissioner, as the case may be, does not make a reference or pass an order within the specified time, then the option for safe harbor exercised by the assessee shall be treated as valid.

Scope of definitions

The scope of Operating Revenue and Operating Expense to be used in the computation of the Operating Margin has been clearly defined in the Safe Harbour Rules.

Navigating the Safe Harbour Application process doesn’t have to be overwhelming. We’re here to provide discreet and effective assistance every step of the way.

SBC support:

met inter alia made the following recommendations relating to changes in GST tax rates, measures for facilitation of trade and measures for streamlining compliances in GST.

RCM applicability on

SBC Comments:

Earlier, w.e.f. 18th July 2022, the renting of residential property was subject to Reverse Charge Mechanism (RCM). The proposal now suggests extending RCM to include the renting of commercial property. However, the term “commercial property” has not been explicitly defined in the law. It is also proposed that all types of commercial property rentals may eventually be brought under the purview of GST

Reverse Charge Mechanism (RCM) to be introduced on supply of metal scrap by unregistered person to registered person provided that the supplier shall take registration as and when it crosses threshold limit and the recipient who is liable to pay under RCM shall pay tax even if supplier is under threshold.

A TDS of 2% will be applicable on the supply of metal scrap by a registered person in B-to-B supply

SBC Comments:

Previously, the applicability of Tax Deducted at Source (TDS) was restricted to government companies and their related entities. As this metal scrap industry is an unorganized sector. It is now proposed that a 2% TDS will be imposed on the business-to-business (B2B) supply of metal scrap.

Introduction of a Reverse Charge Mechanism (RCM) ledger, an Input Tax Credit Reclaim ledger (by 31 October 2024) and an Invoice Management System (IMS)

SBC Comments:

The Reverse Charge Mechanism (RCM) ledger and Invoice Management System (IMS) streamline compliance on the GST portal by allowing to manage of regular ITC and RCM ITC while also providing tools for effective invoice management.

SBC Comments:

B2B E-invoicing compliance was introduced on October 1, 2020. It was mandatory for businesses with a turnover exceeding INR 500 crore or more, which was gradually brought down to INR 5 crore or more. However, due to the large volume of transactions, B2C E invoicing is also being considered. The specific limits for B2C E-invoicing are currently under discussion and will be notified soon.

Constitute a Group of Ministers (GoM) to holistically look into the issues pertaining to GST on life insurance and health insurance. The GoM is to submit the report by end of October 2024.

Location charges or Preferential Location Charges (PLC) paid along with the consideration for the construction services of residential/commercial/industrial complex before issuance of completion certificate forms part of composite supply

SBC Comments:

This clarification comes as a much-needed relief for the real estate industry, addressing the long-standing ambiguity regarding tax rates on Preferential Location Charges (PLC). For buyers, this is great news! Instead of the GST rate of 18% being applied to PLC, it will now be taxed at a reduced rate of 5%, or 1% for affordable housing.

When a Goods Transport Agency (GTA) provides additional services (like loading, unloading, packing, unpacking, transshipment, or temporary warehousing) during the transportation of goods by road and issues a consignment note, these services are considered part of a composite supply.

If these services are provided separately and invoiced separately, they are not treated as part of the composite supply of transportation of goods

The GST Council recommended the early notification of sections 118 and 150 of the Finance (No. 2) Act, 2024, which introduce sub-sections (5) and (6) into section 16 of the CGST Act, 2017, with retrospective effect from July 1, 2017. They also suggested a special procedure for rectifying orders under section 148 of the CGST Act for taxable persons who received orders for wrong input tax credit claims but are now eligible under the new sub-sections. Additionally, a circular will be issued to clarify the procedure and address issues related to these new provisions.

SBC Comments:

A retrospective amendment of sub-sections (5) and (6) into section 16 provides great relief to the taxpayers who were affected by delayed claiming of ITC. They can now avail the benefit of it by approaching the appropriated appellate authority for revision of orders.

The GST Council recommended that, where the inputs were initially imported without payment of IGST and compensation cess by availing benefits under Notification No. 78/2017-Customs dated 13.10.2017 or Notification No. 79/2017-Customs dated 13.10.2017 are later paid along with interest, the refunded IGST on exports will not breach Rule 96(10) of the CGST Rules. To ease the refund process for exporters, the Council also suggested the prospective removal of Rules 96(10), 89(4A), and 89(4B) from the CGST Rules, 2017.

SBC Comments:

Exporters who fulfill the conditions of paying IGST and compensation cess on imported inputs (along with interest) and having the Bill of Entry reassessed will no longer be required to repay the refunded IGST with interest and penalties under Section 74.

However, many exporters have already incurred penalties, including repayment of the IGST refund, interest, and additional penalties ranging from 15% to 100%.Many taxpayers were unable to claim refunds due to restrictions imposed under Rule 96(10). This is a huge relief given to the exporters with payment of tax.

The GST Council recommended adding rule 164 to the CGST Rules, 2017, to outline the procedure and conditions for waiving interest or penalties on tax demands for FYs 2017-18, 2018-19, and 2019 20 under section 128A of the CGST Act. They also recommended that the insertion of section 128A (Amnesty Scheme) in CGST Act, 2017, may be notified with effect from 01.11.2024. and related circulars along with

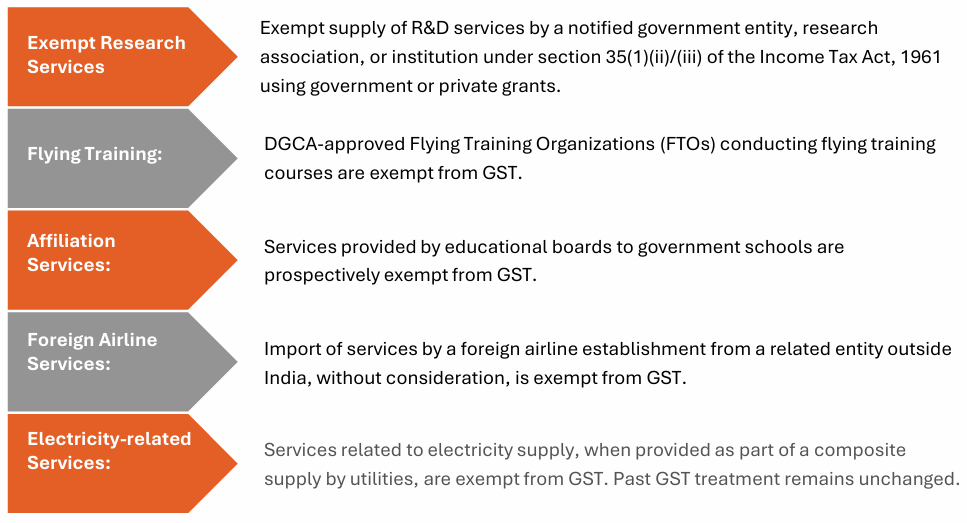

a. Place of Supply for advertising services provided by Indian companies to foreign entities.

b. Availability of Input Tax Credit on demo vehicles for vehicle dealers.

c. Place of Supply for data hosting services provided by Indian service providers to foreign cloud computing service provider

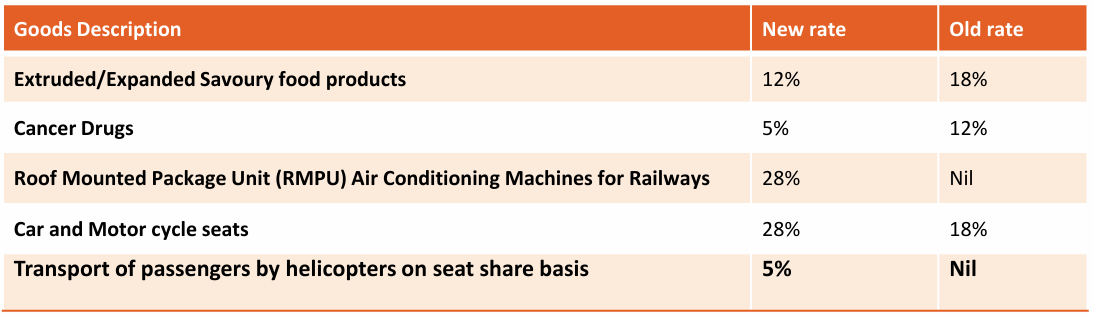

Changes in GST Rates on Goods & Services:

For cases with disputed tax, interest charged or chargeable and penalty levied or leviable

*Settlement amounts payable to be reduced to 50% in following cases:-Where appeal/writ/Special leave petition is filed by the tax authorities.-The Appellant’s case is favorably covered by the ITAT/High Court decision in taxpayer’s own case.

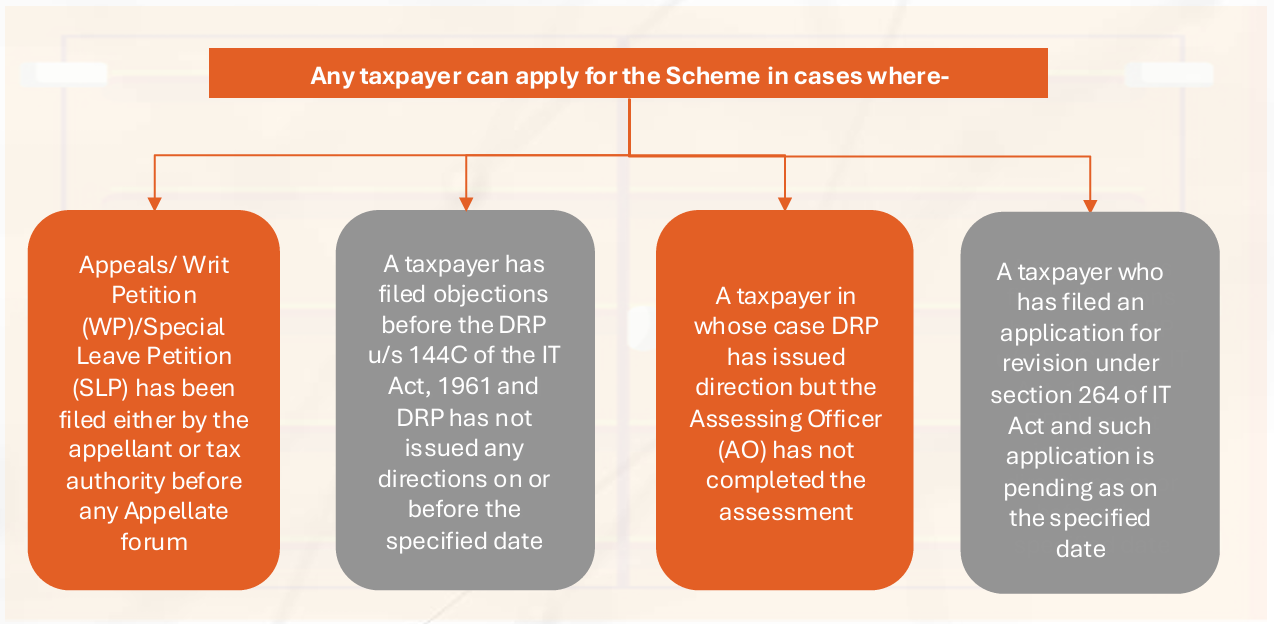

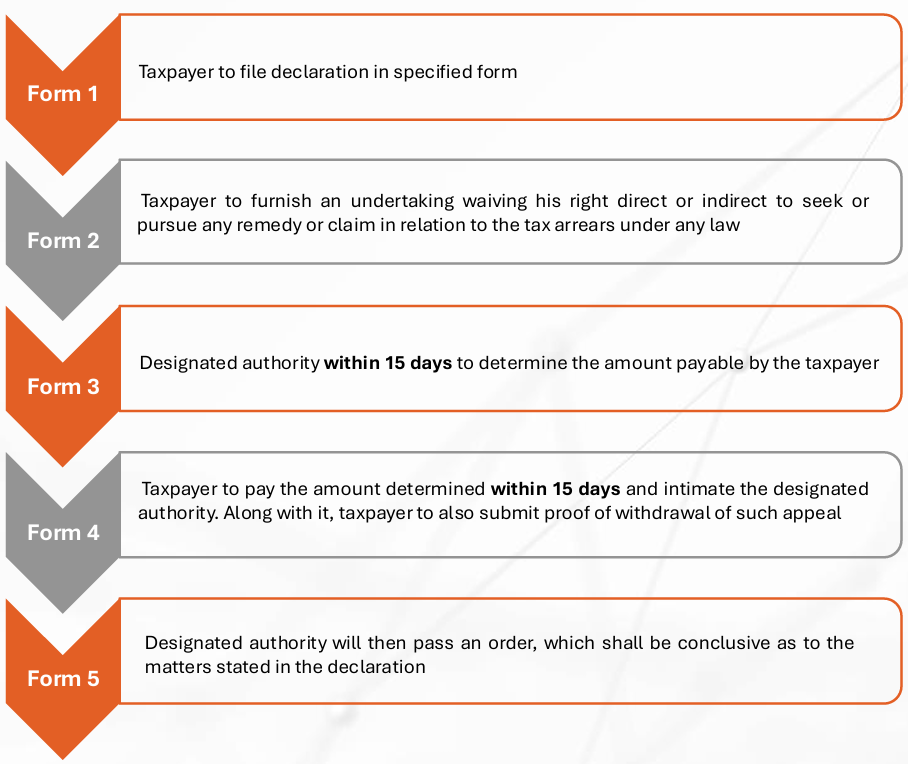

Any Assessee opting for the scheme shall follow the following procedure as specified in the guidelines

• The above forms are further discussed in the ensuing slides. The above forms are based on the DTVSVS 2020 Scheme and the Forms for DTVSVS 2024 scheme are yet to be notified. However, given the similarity in the schemes, there may be minor changes in the fields and format of the Form while the essence remaining intact

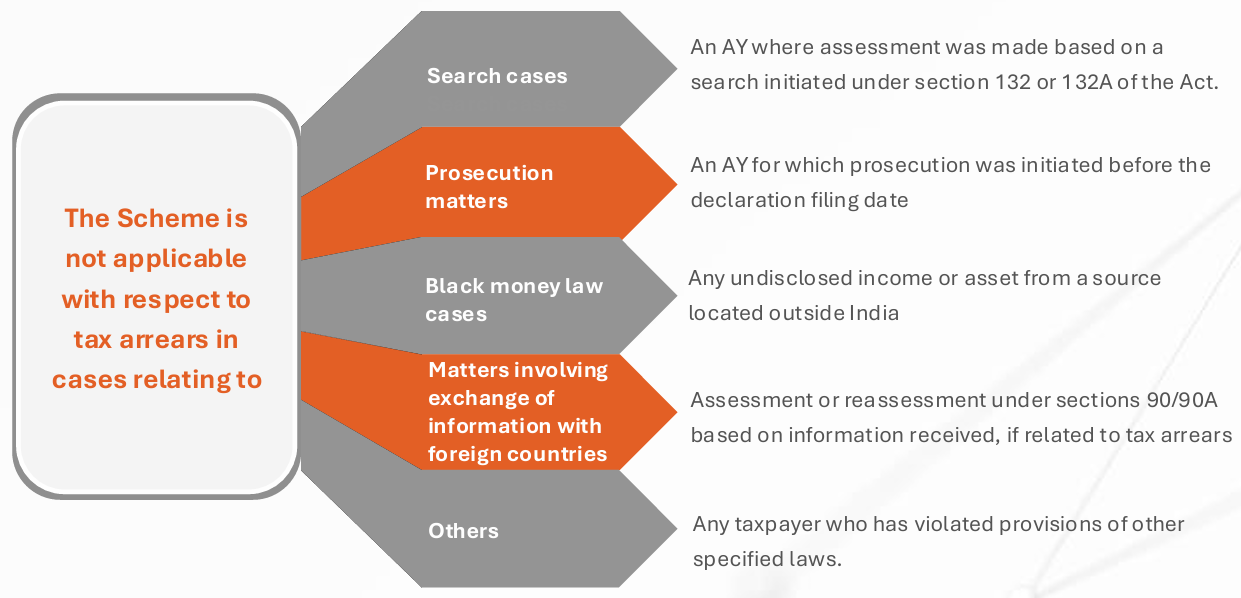

Important: The declaration under the Scheme shall be deemed not to have been made if,–

(a) any material particular furnished is found to be false at any stage; or

(b) Violation of conditions of the Scheme; or

(c) the declarant acts in any manner which is not in accordance with the undertaking given by him.

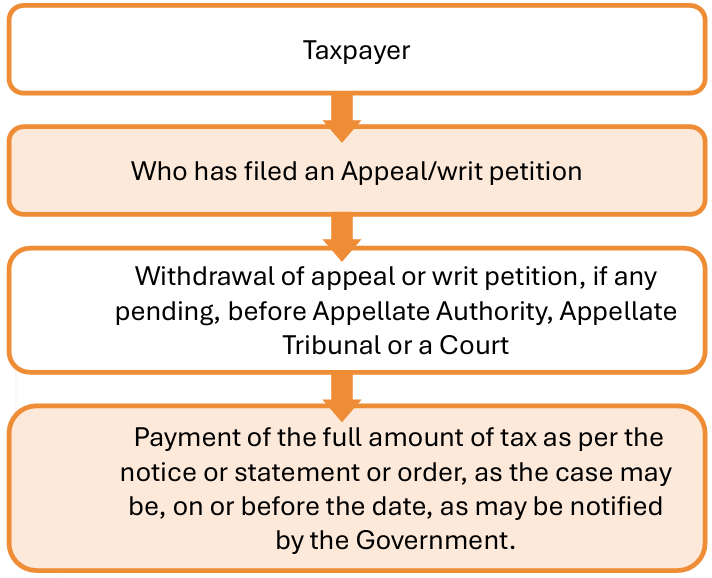

All the proceedings and claims which were withdrawn under this section and all the consequences under the Income-tax Act against the declarant shall be deemed to have been revived.

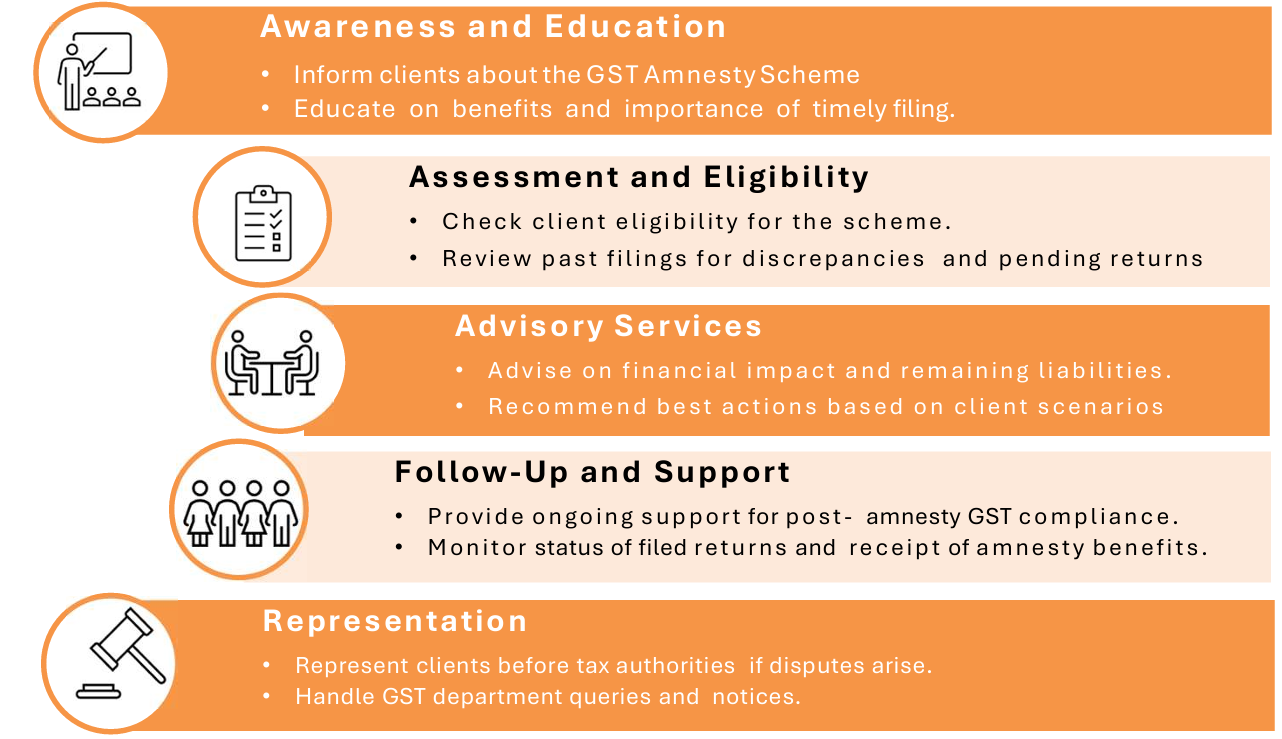

Previously (as examples shown below) are amnesty schemes under the CBIC which have typically addressed issues related to the late submission of GST monthly and Annual Returns. These initiatives aimed to alleviate penalties and encourage compliance among taxpayers. Similarly, The latest scheme, discussed in the 53rd GST Council meeting and

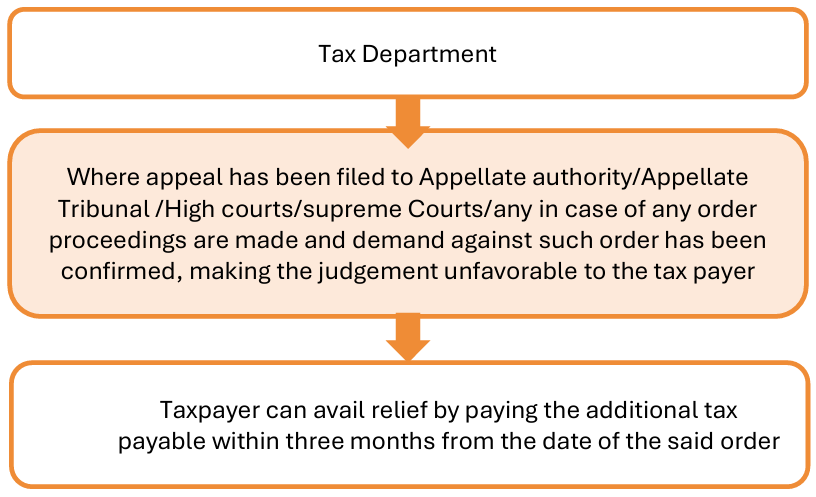

detailed in the financial bill, 2024, introduces Section 128A in CGST Act to provide conditional waiver of interest or penalty or both relating to demands raised under section 73 years 2017-18, 2018-19 and 2019-20 , in cases where demand notices have been issued under section 73and full taxliability is paid by the taxpayer before a date to be notified.

Scope: Applies specifically to demands under Section 73, which generally deals with non-fraudulent tax discrepancies and refunds.

Time Frame: Relief applicable for tax periods from FY2017-18 to FY2019-20.

Due Date for Payment: All taxes must be paid on or before March 31, 2025 as per the 53rd GST Council meeting. However, currently the law remains silent and an official notification from the government is yet to be issued.

Relief: Complete waiver of interest and penalty.

While the proposed GST Amnesty Scheme under Section 128A offers significant relief to taxpayers, it is important to understand that certain cases are noteligible for this scheme. This exclusion aims to maintain the integrity of the tax system and ensure that the scheme benefits those who comply with the law in good faith. The following are the key

exclusions:

The applicability extends to:

ii. Issued right afterward if there is a need to formally demand the payment of the tax assessed in ASMT

10.)

A. Acceptance of all allegations – Pay the demanded tax amount and avail benefits of section 128A i.e– waiver of interest and penalty.

B. Acceptance of some of the allegations – Pay tax, interest and penalties attracted towards accepted allegations.

C. Declination of all the allegations – Go for further proceedings or pay the pre-deposit for further appeals.