1. Roadmap for pursuit of Viksit Bharat

Macro Fiscal Cues:

• Inflation – Low and stable, moving towards the 4% target. Core inflation (non-food, non-fuel) at 3.1%.

• Total Receipts – Estimated at ₹32.07 lakh crore(excluding borrowings).

• Total Expenditure – Estimated at ₹48.21 lakh crore.

• Net Tax Receipts – Estimated at ₹25.83 lakh crore.

• Fiscal Deficit – Estimated at 4.9% of GDP, with a goal to reduce it below 4.5% next year.

Future Fiscal Strategy – From 2026-27 onwards, the aim is to ensure the fiscal deficit keeps Central Government debt on a declining path as a percentage of GDP.

2. Direct Tax Proposals

Revamped Act on its way

“I am now announcing a comprehensive review of the Income-tax Act,1961. The purpose is to

• make the Act concise, lucid, easy to read and understand

• reduce the disputes and litigation

• provide certainty to taxpayers”

It will also bring down the demand embroiled in litigation. It is proposed to be completed in six months.”

i. Individuals

Above change results in savings of ₹17,500 to the individual taxpayers opting for New Regime

Other Key Proposals:

• Standard deduction under Section (u/s) 16 increased from ₹50k to ₹75k under the New Regime (Not eligible for Old Regime)

• Deduction for Employers’ contribution u/s 80CCD towards Pension scheme opting for New Regime increased from 10% to 14% of employee’s basic salary

• TCS paid by employees for the purpose of computing TDS required to be withheld from salary w.e.f. 01-Oct-2024 which was not previously allowed to be set off resulting in a tax refund situation

• W.e.f. 01-Oct-2024 under the Black Money and Imposition of Tax Act, 2015, failure to report/inaccurate reporting of foreign incomes / overseas assets will attract a penalty if the value of foreign assets does not exceed ₹20 lakhs u/s 42 and 43 (Previously the limit was ₹10 lakhs with an exception to the bank account(s) not exceeding ₹5 lakhs)

• TCS credit of the minor shall only be allowed where the income of the minor is being clubbed with the parent as under sub-section (1A) of section 64 of the Act

SBC Comments:

The Finance Bill 2024 proposes amending the slab rates while maintaining a baseline exemption of INR 300,000. It also increases the standard deduction for salaried taxpayers from INR 50,000 to INR 75,000, which provides only minimal tax benefits.

Although these amendments fall short of expectations, they represent a welcome step towards providing much-needed relief for individuals.

ii. Corporates

As per the information provided, 58% of corporate tax in FY 2022-23 was collected under the new corporate tax regime. Thereby, there are no changes proposed for Corporates and the old rates shall continue to apply as per the applicable regime.

Other updates apart from Transaction-related amendments are as follows:

a) Foreign Companies:

• Corporate tax rate for foreign companies reduced from 40% to 35%. ETR of 38.22% (including surcharge and health and education cess)

SBC Comments:

Reduction of corporate tax rate for foreign companies is anticipated to reduce the tax on business income and other income (not addressed by any specific provisions of the IT Act or treaty) of foreign companies, arising from their business connection or permanent establishment in India.

b) Pillar One and Pillar Two:

Withdrawal of the Equalisation Levy (EL) of 2% introduced in 2020.

• Hon’ble Finance Minister explained the rationale behind the withdrawal of EL of 2%. She stated that EL withdrawal is in the interest of moving towards Pillar One and Pillar Two.

• Consideration received or receivable for e-commerce supplies or services on or after this date will not be subject to the EL of 2%.

• However, EL of 6% on Online Advertisement Services shall continue.

SBC Comments:

There were hopes that this Budget might outline a roadmap for implementing the OECD’s Two Pillar framework in India. In this context, the withdrawal of the EL could have been seen as a preparatory step towards adopting the Two Pillar solution. However, the budget documents make no mention of Pillar 2 rules. The stated rationale for withdrawing the EL is not its alignment with the Two Pillar solution but rather concerns about the levy’s scope and compliance burden. It seems India is maintaining a wait-and-see approach regarding the Two Pillar Solution.

c) Submission of a statement by the liaison office of NR in India:

• NRs having a liaison office in India are required to prepare and deliver a statement in respect of its activities in a financial year to AO. New Section 271GC proposed for levy of a penalty of ₹ 1,000 for every day of failure to furnish such statement unless it proves to have reasonable cause.

d) Disallowance u/s 37:

• Expenditure incurred by an Assessee for any purpose which is an offence or which is prohibited by law shall include any expenditure incurred to settle proceedings initiated in relation to a contravention under any law.

• These expenses incurred on settlement in relation to a contravention under any law are to be notified by the Central Government, w.e.f. FY 2024-25.

SBC Comments:

Courts have ruled that settling a dispute is based on commercial expediency and business interests, aimed at ensuring the Assessee can continue its business operations without interruption. Consequently, any amount paid to settle a dispute was previously permitted as a business expense under Section 37(1) of the IT Act. However, with the addition of clause (iv) to Explanation 3 of Section 37(1), no deduction will now be allowed for expenditures incurred to settle such proceedings.

e) Taxation of domestic cruise ship operations by non-residents

• New presumptive taxation regime introduced for domestic cruise ship operations & exemption on lease rental in the hands of immediate NR sister company till FY 2029-30

• 20% of revenue of the NR operator, on account of carriage of passengers to be deemed as business income. Existing presumptive taxation regime for the shipping business of NR will not be applicable for NR’s domestic cruise operators.

SBC Comments:

India’s potential for cruise tourism is enhanced by its extensive coastal and riverine infrastructure. Additionally, the growing tourism in destinations such as Lakshadweep and other islands is anticipated to further boost the cruise tourism sector. Moving forward, foreign cruise shipping companies will have the option to choose a tax rate of 20%.It is important to note that previously, non-residents involved in shipping, including cruise shipping, were eligible for a presumptive tax rate of 7.5% on their total income.

iii. Trusts/Institutions

a) Merger of trusts under the first regime with the second regime:

• W.e.f 01-Oct-2024 applications for approval u/s 10(23C) shall be considered as per the provisions of Sections 11 and 12.

b) Condonation of delay in filing application for registration by trusts or

institutions:

• A trust or institution desirous of seeking registration under section 12AB is required to apply within timelines specified in clause (ac) of sub-section (1) of section 12A.

• It is proposed that the Principal Commissioner/ Commissioner may be enabled to condone the delay in filing applications and treat such applications as filed within time to help the genuine cases of delay.

• Similar provisions provided for Section 80G related application

c) Timeline for disposing of applications u/s 12AB and 80G provided:

• W.e.f. 01-Oct-2024, the timeline shall be six months from the end of the quarter in which the application was received

d) Donations to the National Sports Development Fund

• Any sums paid by the Assessee in the previous year as donations to the National Sports Development Fund set up by the Central Government shall be eligible for deduction for other taxpayers u/s 80G.

• Thus, such a fund can claim the benefit of donations accordingly as per Section 11 and 12 as well.

SBC Comments:

The alignment of both regimes and the proposed gradual transition to the second regime reflect a push towards procedural simplification and reduced administrative burden, ensuring a smoother and more efficient framework.

Care must be taken to ensure that the transition does not disrupt operations and claim of exemption/benefits. This requires clear guidance and support to the Trusts/such institutions for its tax matters.

iv. Partnership Firms

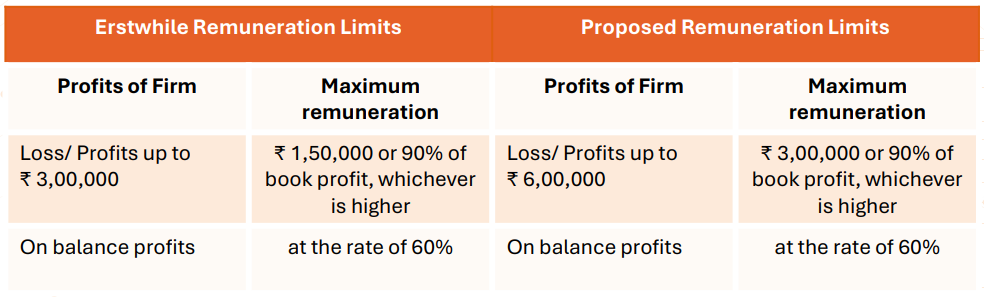

a) Increase in limit of remuneration to working partners of a firm allowed as deduction:

b) Other updates:

• Section 194T has been introduced to provide 10% TDS by the firm on payment salary, remuneration, commission, bonus or interest to a partner.

• Limit of ₹ 20,000 applicable for TDS chargeability u/s 194T in an FY.

• TDS to be deducted on payment/ accrual or transfer to partner’s capital account. Withholding obligations continue even on interest/ salary payments above specified limits

• No changes in the tax rates for the partnership firms as was expected in line with new regimes introduced for individuals, companies, co-operative society etc.,

Amendment applicable ideally from FY 2024-25

SBC Comments:

The proposed amendment to increase the deduction limit for working partners’ remuneration is a positive development, offering greater flexibility by allowing up to Rs 3,00,000 or 90% of the book profit on the first Rs 6,00,000 of profit or in the case of a loss. This change could enhance tax benefits for partnership firms and improve financial flexibility.

v. Capital Gains

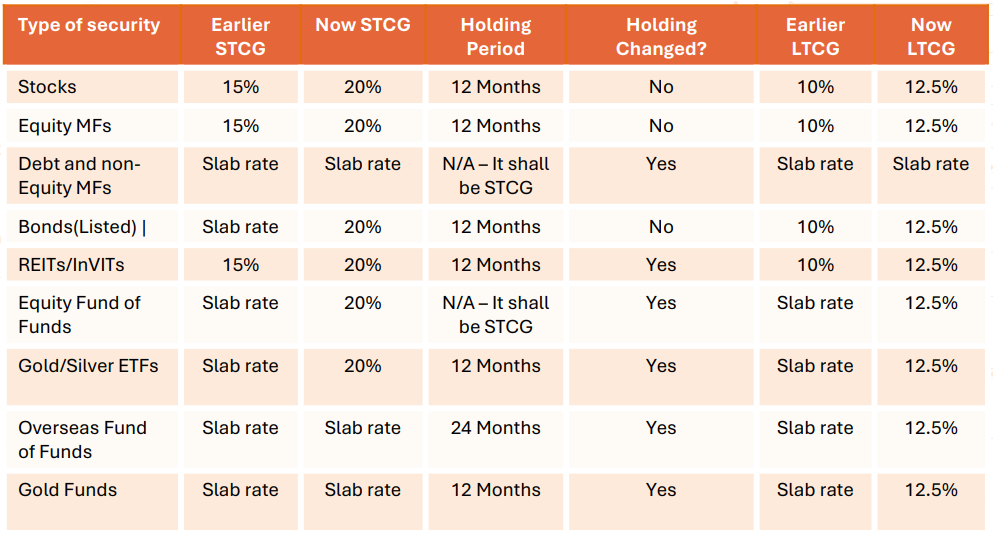

a) Revised period of holding and rates for all Listed Securities:

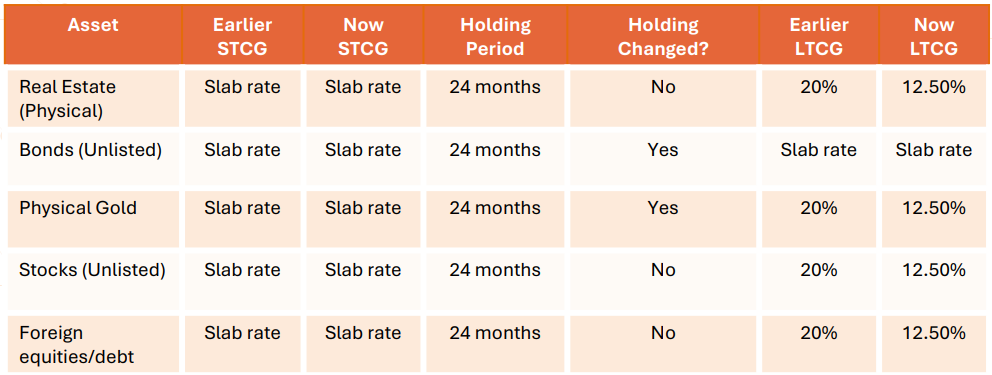

b) Revised period of holding and rates for Unlisted Assets:

Currently, STCG is taxed @ 15% or the applicable slab rate and LTCG are taxed at 10% or 20%, depending on the residential status of the taxpayer and category of asset. However, w.e.f. 23-Jul-2024, STCG has been raised from 15% to 20% on specified assets. Other STCG shall continue to be taxed at the applicable slab rate and LTCG will be 12.5%

SBC Comments:

The proposed overhaul of long-term capital gains tax rates suggests a unified rate of 12.5% across all asset categories. Previously, the rate was 10% for STT-paid listed equity shares, units of equity-oriented funds, and business trusts under Section 112A, and 20% for other assets with indexation benefits under Section 112 of the IT Act.

This change equalizes tax rates for listed and unlisted shares, potentially impacting the private equity sector, where companies previously sought IPOs to benefit from the lower 10% tax rate. For promoters, this adjustment may reduce the incentive to use externalization structures for tax planning.

The present rate of tax of 15% for STCG was considered to be very low and largely benefitted the High-net-worth individuals. Increased tax on capital gains could reduce ROI and diminish some appeal of the booming Indian stock market. However, it does rationalize long-term capital gains taxation, addressing the previous disparity where residents faced higher rates compared to non-residents.

c) Key LTCG and Securities Transaction Tax takeaways:

• No indexation benefit in the case of any long-term capital assets.

• Increase in rates of STT on sale of an option in securities from 0.0625% to 0.1% of the option premium and on sale of a futures in securities from 0.0125% to 0.02% of the price at which such “futures” are traded.

SBC Comments:

The tax rate on other long-term assets has been lowered from 20% to 12.5%. While this change appears advantageous initially, the elimination of the indexation benefit could significantly impact taxpayers.

Indexation adjusts the asset’s purchase price for inflation, reducing the taxable capital gain. Without this adjustment, the entire gain is taxable, which could be a heavy burden, particularly when the return on investment vis-à-vis inflation there is disparity.

Further, on increase in STT, for the Futures and Options segment STT has nearly doubled, and the tax advantage of buybacks over dividends has been eliminated. While this may cause some short-term disruption in the stock market, history shows that such changes are often temporary, and the markets are likely to adapt and continue their growth.

d) Shares acquired as part of Offer for sale:

• Taxpayers in some cases are not paying capital gains tax on the transfer of shares acquired through the Offer for Sale (OFS) route citing the absence of an express provision for the determination of the FMV.

• The contention taken by taxpayers was that since they were still unlisted on the date of transfer even though STT has been paid on transfer and thus, the Cost of Acquisition is indeterminable, and Capital Gains is not chargeable.

• Section 55 amended to provide Mechanism to determine the cost of acquisition of equity shares acquired before February 1, 2018, and transferred as part of the Offer for Sale

Fair Market Value = Original cost of acquisition * (Cost Inflation Index for the financial year 2017-18)/(Cost Inflation Index for the 1st year in which the asset was held by the Assessee or for the year beginning on the 1st day of April 2001, whichever is later)

SBC Comments:

Previously, taxpayers used various methods to compute the cost of acquisition for shares offered under an OFS, including original cost, indexed cost, FMV based on valuers’ reports, or even arguing that the transaction wasn’t taxable due to computation issues. The proposed amendment aims to clarify this issue definitively. As it is a retrospective change, those who adopted aggressive positions will need to reassess and potentially revise their returns.

e) Gains from unlisted bonds and debentures:

• Gains from unlisted bonds and debentures transferred, redeemed or maturing on or after 23 July 2024 will be treated as STCG irrespective of the holding period.

SBC Comments:

Unlisted debentures and bonds are set to be taxed according to the rates specified under Section 50AA of the IT Act. Consequently, these instruments will not benefit from the reduced long-term capital gains tax rate.

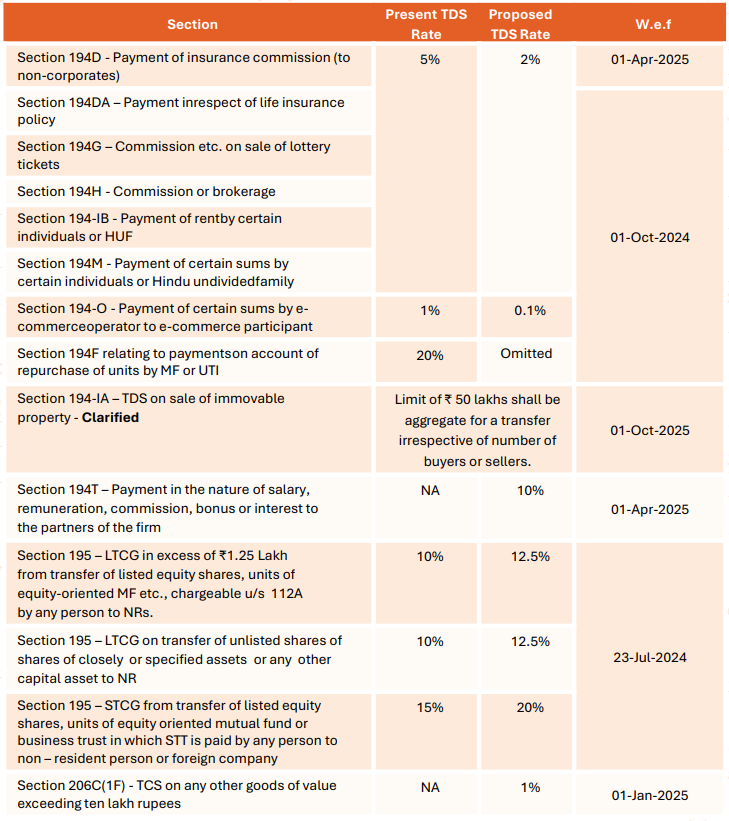

vi. TDS/TCS Rates

a) Rationalisation of TDS/TCS rates:

SBC Comments:

The proposed amendments seek to rationalize TDS rates by lowering them on various provisions, which is expected to ease cash flow impacts. This change aims to enhance business efficiency and improve compliance.

The current rationalization is the first baby step which the Government has already taken towards simplification of the direct tax laws in India aiming to provide ease of business and certainty to the taxpayers and making India more attractive destination for FDI/Investments.

Apart from the above, it is to be noted that TCS has introduced on luxury expenses. The proposed expansion of this section to include any notified luxury goods will enhance the tracking of related expenses. Effective from January 1, 2025, this amendment is likely to improve transparency and ensure better compliance with expenditure regulations.

b) Scope of 194C to exclude payments u/s 194J:

• It is proposed to explicitly state that sum paid and liable u/s 194J does not constitute “work” for the purposes of TDS under section 194C. This is to provide certainty on the treatment of payments u/s 194C vis-à-vis 194J.

SBC Comments:

The proposed amendment clarifies that Section 194C does not apply to (i) transactions where TDS is deductible under Section 194J, or (ii) manufacturing or processing based on customer specifications when the material for manufacturing

or processing is not supplied by the customer or their associates.

c) Time limit for revision of TDS/TCS returns:

• Correction statements can be filed on TRACES/offline only within 6 years from the end of FY in which such TDS/TCS statements were filed.

SBC Comments:

Such statements could be revised repeatedly and indefinitely, potentially leading to misuse of these provisions and causing difficulties for deductees and collectees. Thus, this has been introduced to provide certainty and to avoid unwarranted litigation.

d) TCS suffered by employees to be considered for TDS deduction:

• Employers may now consider TCS suffered by employees when calculating TDS on employee salary payments w.e.f 01-Oct-2024.

e) Processing of statements other than those filed by the deductor:

• Scheme for processing of statements shall be made for filing by persons other than deductor viz., Form No. 26QF which is filed by an Exchange wherein the deductee is filing details of the tax

f) Lower TDS/TCS certificate for 194Q and 206C(1H):

• Lower TDS/TCS applications can now be filed for payments liable

– for TDS u/s 194Q for purchase of goods

– for TCS u/s 206C(1H) on sales of goods

g) Penalty for failure to furnish TDS/TCS statements:

• Time limit for not levying penalty u/s 271H reduced from 1 year to 1 month from the due date to ensure better compliance.

h) Time limit to pass order for failure to deduct/ collect or pay TDS/ TCS:

• The existing provision of Section 201(3) in the IT Act provided a time limit of 7 years for deeming a person to be an ‘Assessee in default’ for failure to deduct tax from a resident, whereas no time limit was prescribed in case of failure to deduct from a non-resident.

• Further there are no limits specified for passing an order under section 206C of the IT Act.

• It is proposed to amend section 201(3) to amend the time limit to 6 years for issuance of order deeming a person to be an ‘Assessee in default’, for failure to deduct part or whole of tax from any person, i.e., a resident and a nonresident.

• Further, it has been proposed to insert Section 206C(7A) providing that no order shall be made by deeming a person as an ‘Assessee in default’ in case of failure to collect tax after expiry of six years from the end of the financial year in which tax was collectible or two years from the end of the financial year in which the correction statement is delivered under sub-section (3B), whichever is later

SBC Comments:

All lacunae and shortfalls in the provisions are being addressed, which will enhance the operations of both taxpayers and tax authorities

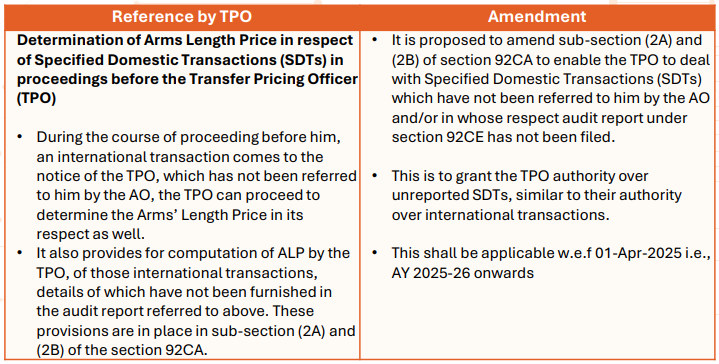

vii. Transfer Pricing

Other key points to be noted from the Finance Minister’s Speech:

a) With a view to reduce litigation and provide certainty in international taxation, CBDT will

• expand the scope of safe harbour rules and make them more attractive.

• streamline the Transfer Pricing (TP) assessment procedure.

It is exciting to see that the TP amendments have begun towards the extended vision of making the direct tax structure more certain. It would make India an attractive hub for more investments and further its growth story.

b) Vivad Se Vishwas Scheme, 2024 mechanism will ideally apply for TP adjustments and thereby enable expeditious disposal of pending disputes/litigations for TP litigations.

c) Interest limitation rules u/s 94B not to apply to financial companies operating in IFSC while other tax exemption framework proposed for Retail schemes and ETFs set up in IFSC

SBC Comments:

The amendment provides the authority to the TPO to determine ALP even if SDT are not reported in Form 3CEB.

viii. Transaction tax

a) Abolition of Angel Taxation i.e., fair value in excess of share premium abolished

• Issue of shares by closely held companies above FMV was liable to Angel Tax for the company issuing the shares. These provisions are proposed to be omitted from FY 2024-25 (AY 2025-26).

• Thus, the excess premium received by a company on the issue of shares shall no longer be taxable in the hands of the company as ‘Income from Other Sources’.

SBC Comments:

The proposed abolition of the Angel Tax represents a major milestone for domestic companies that have grappled with legal and practical issues under these contentious provisions. Historically, the Angel Tax led to disputes over valuation methodologies, treatment of estimated figures, scrutiny of funding sources, and taxation of equity conversions. Initially designed to curb black money, it ended up being used to tax shares issued above fair market value, resulting in extensive litigation and complications, especially for non-resident investors dealing with conflicting regulations (Exchange Control Regulations vs. IT Act) from FY 2023-24.

The Finance Minister’s decision to eliminate the Angel Tax (Section 56(2)(viib) of the IT Act) for all shareholder classes is a significant move towards increasing tax certainty, reducing litigation, and supporting the startup ecosystem. This change is expected to lessen burdens on investors, simplify deal negotiations, and streamline documentation processes. It also highlights the government’s commitment to fostering growth and innovation, enhancing the resilience and productivity of key sectors in the evolving economic landscape.

b) Corporate gifting of shares etc., to be taxable:

• It is now proposed to allow only gifts out of natural love and affection u/s 47 as not transfer and thus, not liable to tax.

• Tax positions of non-chargeability for corporate gifting can no longer be used.

SBC Comments:

The availability of benefits under Section 47 of the IT Act for transactions involving gifts from unnatural persons (e.g., transfer of shares by corporates at no consideration) has historically led to contention and litigation.

The proposed amendment to Section 47(iii) of the IT Act will apply prospectively. It will be important to assess the impact on transactions involving gifts by unnatural persons conducted before the new provisions take effect, especially in light of previous judgments on the matter.

c) Slump sale to be taxed as per the reduced period:

• Period of holding reduced to 24 months from 36 months to qualify for lower of tax on LTCG as a result of slump sale.

SBC Comments:

Slump sale may be structured for the reduced period enhancing the possibility of claim of LTCG on account of the reduced period.

d) Reduction of tax on foreign companies from 40% to 35% to benefit sale of unlisted shares

• Unlisted shares held for a period of less than 24 months shall be taxed at reduced rate of 35%

SBC Comments:

Reduction of corporate tax rate for foreign companies is anticipated to reduce the tax on business income and other income (not addressed by any specific provisions of the IT Act or treaty) of foreign companies, arising from their business connection or permanent establishment in India.

e) Taxation of Buy-back of securities:

• Any sum received by shareholders on buyback of shares shall be treated as dividend income in the hands of shareholders and shall be taxable at applicable rates.

• No deduction for expenses shall be available against such dividend income.

• Further, the cost of acquisition of shares bought back will be treated as a capital loss and shall be available for set-off / carry forward against other capital gains income as applicable.

• The amendment shall be applicable w.e.f. 01-Oct-2024

SBC Comments:

In the case of buy back, it remains unclear and has created ambiguity for many scenarios wherein the genuine cost of acquisition is not available for claim or set off against the amount received on buy-back.

Buy-back is a case of extinguishment of right in asset and the current provisions are void of this understanding while impacting the cash repatriation strategies through buy-back of shares.

viii. Litigation

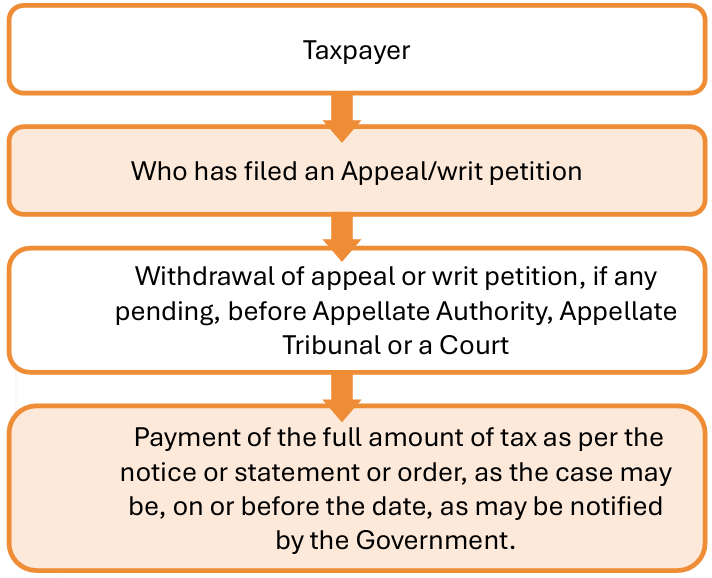

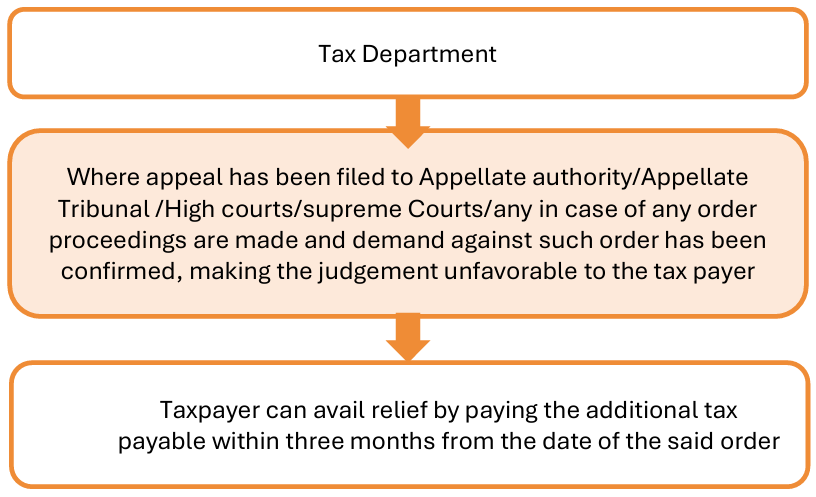

a) Vivad se Vishwas Scheme, 2024:

• Keeping in view the success of the previous Vivad Se Vishwas Act, 2020 and the mounting pendency of appeals at the CIT(A) level, the introduction of a Direct Tax Vivad se Vishwas Scheme, 2024 is proposed which is yet to be notified. The objective is to provide a mechanism for the settlement of disputed issues, thereby reducing litigation without much cost to the exchequer.

Where the tax department is in appeal or the disputed issue has already been decided by in favour of the declarant by a higher appellate forum, namely ITAT, High Court or the Supreme Court and is not overturned, the amount payable by the declarant shall be one-half of the amounts specified in column (4) and (5) of the above table (as applicable). The method of computation in such cases will be prescribed by the Government.

a) Vivad se Vishwas Scheme, 2024 (continued):

• The Scheme is applicable to an ‘appellant’, which would include the following person in whose case an appeal or a writ petition or special leave petition has been filed either by him or by the income-tax authority or by both; or objection before DRP or revision application u/s 264 has been filed by the person. Further such respective appeal or petition or DRP direction or application u/s 264 is pending or DRP direction has been issued and pending for give effect order by AO as on 22nd July 2024.

• Other conditions are similar to earlier scheme of 2020: a) Declaration has to be filed before designated authority b) Appeals are to be withdrawn and other remedies/claim are to be waived by the Appellant c) Neither the authorities nor the declarant can contend that the declarant�appellant or the authorities, as the case may be, has acquiesced in the decision on the disputed issue by settling the dispute.

• Timelines under the above proposed Scheme:

Designated authority to determine the amount payable by the declarant within 15 days of filing the declaration. Thereafter, the declarant is to make payment and furnish proof thereof within 15 days thereafter.

• Exclusions from VSV Scheme where tax arrears relate to:

• Search cases

• AY for which prosecution is instituted before filing declaration

• Undisclosed foreign income and assets.

• Where assessment has been made on the basis of information from foreign countries

• Prosecution cases filed by the Department for offences punishable under the Bharatiya Nyaya Sanhita, 2023 or for the purpose of enforcement of any civil liability under any law for the time being in force, on or before the filing of the declaration or such person has been convicted of any such offence consequent to the prosecution initiated by an Income

tax authority.

• Prosecution has been initiated under Narcotic Drugs and Psychotropic Substances Act, Special Courts Act, the Unlawful Activities (Prevention) Act 1967, the Prevention of Corruption Act, the Conservation of Foreign Exchange and Prevention of Smuggling Activities Act 1974, the Prevention of Money Laundering Act 2002, the Prohibition of Benami Property Transactions Act, 2016 on or before filing of the declaration or such person has been convicted of any such offence punishable under any of those Acts.

SBC Comments:

The rising backlog of litigation, with appeals increasing faster than disposals, highlights the need for effective dispute resolution.

Building on the success of the Vivad Se Vishwas Act, 2020, the proposed Direct Tax Vivad Se Vishwas Scheme, 2024 aims to address this issue by offering a streamlined mechanism for settling disputes. This initiative is expected to reduce litigation costs and clear the backlog efficiently, benefiting both taxpayers and the tax administration.

A thorough analysis must be undertaken by the Taxpayers wherein they fall within the definition of the Appellant for the scheme and avail to save efforts and costs invested on litigating the matters.

b) Monetary limits for filing appeals increased for the department:

• The monetary limits for filing appeals related to direct taxes, excise and service tax in the Tax Tribunals, High Courts and Supreme Court have been increased to ₹ 60 lakh, ₹ 2 crore and ₹ 5 crore respectively.

c) Reporting of income from letting out of house property under ‘Income from House Property’

• Overriding the Supreme Court Decision in the case of Chennai Investments it is proposed to amend the section 28 of the Act.

• Thus, any income from letting out of a residential house or a part of the house by the owner shall not be chargeable under the head “Profits and gains of business or profession” and shall be chargeable under the head “Income from house property”.

SBC Comments:

The Supreme Court’s rulings in Chennai Properties & Investments Ltd. and Rayala Corporation (P.) Ltd. established that rental income should be classified based on the primary business intent, either as “business income” or “Income from House Property.”

Recent decisions by high courts have varied based on specifics, but the Finance Bill, 2024 clarifies that income from renting out a residential house will now be taxed as “Income from House Property.” This change specifically targets residential properties and requires developers and landlords to classify rental income accordingly. . In case the let-out unit is classified as a “residential house”, any income from such let out property should be taxed as “Income from

house property”.

d) Monetary limits for filing appeals increased for the department:

• The monetary limits for filing appeals related to direct taxes, excise and service tax in the Tax Tribunals, High Courts and Supreme Court have been increased to ₹ 60 lakh, ₹ 2 crore and ₹ 5 crore respectively.

e) Introduction of block assessment provisions in cases of search:

• ‘Block period’ shall consist of previous years relevant to six AYs preceding the previous year in which the search was initiated.

• Regular assessments for the block period shall abate. There will be one consolidated assessment for the block period. No other regular proceedings shall be done.

• Tax shall be charged at 60% for the block period on the undisclosed income

• No interest under the provisions of section 234A, 234B or 234C or penalty under the provisions of section 270A shall be levied or imposed.

• No access to the DRP during Block Assessments.

• No adjustments allowed for losses, depreciation, or partner payouts

• Penalty at 50% on tax payable for the undisclosed income.

• Time limit for completion of the block assessment 12 months from end of the month in which the authorisations /requisitions were made. Exclusion of 6 months for handing over seized material.

SBC Comments:

The proposed amendment revises the process for handling assessments related to search and seizure proceedings. Under the current scheme, such assessments are conducted under Sections 147 to 151A of the Income Tax Act, which primarily governs reassessments based on new or additional information.

The amendment introduces a distinct procedure specifically for block assessments in cases involving search and seizure operations.

This special procedure aims to streamline the process by separating it from the general reassessment framework.

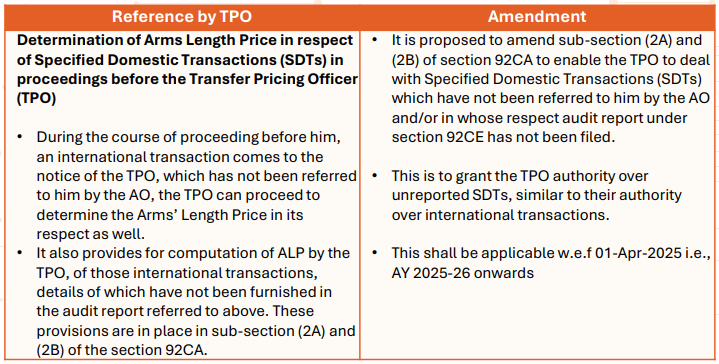

f) Reopening of assessment/reassessments:

• Opportunity of being heard and principle of natural justice further strengthened.

• Information from survey u/s 133A can be used for reassessment. Revised time limits for reopening of assessment shall be as follows:

SBC Comments:

Currently, the time limit applies only to the issuance of notices under Section 148, often resulting in notices under Section 148A being issued close to the deadline for Section 148 notices, leaving insufficient time for adjudication.

The proposed amendment aims to address this by allowing authorities at least three months between issuing a show cause notice and a reassessment notice.

Additionally, the proposed changes will exclude search and seizure proceedings under Section 132 or requisitions under Section 132A from the revised reassessment scheme (Sections 147 to 151A). Instead, a separate block assessment scheme will be introduced for these cases.

g) Advance Rulings withdrawal facilitated:

• Section 245Q proposed to be amended to allow application for withdrawal by the 31-Oct�24 for the transferred applications before Board for Advance Rulings (from AAR) in cases where order u/s 245R has not been passed.

h) Set aside and refer back to AO by CIT(A) in case of Best Judgement Assessment:

• For orders as best judgement case u/s 144 of the Act, CIT(A) shall be empowered to set aside the assessment and refer the case back to the AO for making a fresh assessment.

i) Time limit for completion of assessment, reassessment and recomputation:

• Where ROI is filed as per Condonation order u/s 119(2)(b) – Assessment u/s 143 or 144 can be done within twelve months from the end of the FY in which such return is furnished.

• Time limit introduced for set aside matters by CIT(A) u/s 250.

• The monetary limits for filing appeals related to direct taxes, excise and service tax in the Tax Tribunals, High Courts and Supreme Court have been increased to ₹ 60 lakh, ₹ 2 crore and ₹ 5 crore respectively.

j) Remaining services to be digitized:

All remaining services of Income Tax including rectification and order giving effect to appellate orders shall be digitalized and made paper-less over the next two years.

k) TDS Prosecution

In terms of Section 276B of the IT Act, any person who fails to pay TDS, is punishable with rigorous imprisonment of 3 months to 7 years along with fine.

A proviso is proposed to be inserted whereby, if the payment of such TDS has been made before or at the time of filing of the statement of TDS as required under Section 200 of the IT Act, then the said punishment would not be applicable. This amendment is proposed to come into effect from 01-Oct-2024.

SBC Comments:

This amendment aims to differentiate between a mere failure to report and non-payment of TDS within the prescribed period, and it seeks to decriminalize the former.

TDS Prosecution are most prevalent litigations currently. Thus, introduction of steps to curb the unwarranted litigation for TDS non deposit and prosecution therefrom where there can be genuine reasons for committing such defaults.

3. Indirect Tax Proposals

“To multiply the benefits of GST, we will strive to further simplify and rationalise the tax structure and endeavour to expand it to the remaining sectors.

My proposals for customs duties intend to support domestic manufacturing, deepen local value addition, promote export competitiveness, and simplify taxation, while keeping the interest of the general public and consumers surmount”

– Hon’ble Finance Minister during Budget Speech

i. Customs

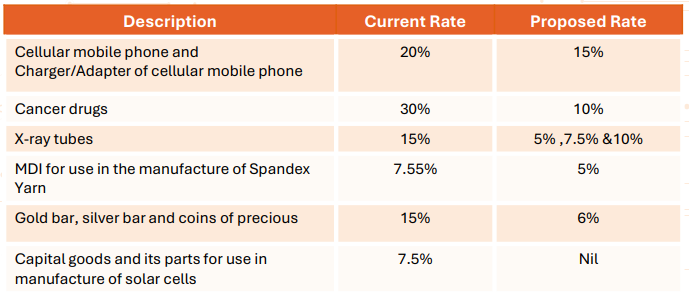

a) Relaxation in Basic Customs Duty (BCD) Rates for certain items:

b) Minerals such as lithium, copper, cobalt and rare earth elements are critical for sectors like nuclear energy, renewable energy, space, defence, telecommunications, and high-tech electronics. Proposal to exempt customs duties on 25 critical minerals.

c) Exemption of Social Welfare Surcharge (SWS) and reduction in Agriculture Infrastructure and Development Cess (AIDC) has been provided for certain goods

SBC Comments:

The Government has undertaken a comprehensive review in respect of 188 conditional exemptions/concessional rates (150 entries in Notification No. 50/2017-Customs dated June 30, 2017 and 38 exemptions/concessional rates in standalone Notifications).

– 30 exemptions/concessional rates are being extended up to 31-Mar-2029

– 126 exemptions/concessional rates are being continued up to 31-Mar-2026

– 28 exemptions/concessional rates are being lapsed on their end dates of 30-Sep-2024 While continuing the exemptions/concessional rates, some entries have been pruned or modified.

d) Ease of compliance:

• Currently, foreign-origin articles can be imported into India for repairs, provided they are re-exported within six months, which can be extended to one year. For aircraft and vessels imported for maintenance, repair, and overhauling, the re-export period has been increased from six months to one year, with a further extension available for an additional year.

• The duty-free re-import period for goods (excluding those under export promotion schemes) exported from India under warranty has been extended from three years to five years, with a possible extension of an additional two years.

• Section 28 DA has been amended to allow for the acceptance of various types of proof of origin as provided in trade agreements, aligning the section with new trade agreements that permit self-certification.

SBC Comments:

The proposed amendments to Section 28DA, which outlines the procedure for claiming a preferential duty rate, aim to expand the types of acceptable proof of origin beyond the traditional certificate of origin. This change aligns with new trade agreements entered into by the Government of India, which include self-certification or declaration by exporters as valid evidence of origin.

A proviso is being inserted to Section 65 (1), providing for manufacturing process or other operations in a warehouse licensed under the MOOWR Scheme. Vide this proviso, the Central Government is empowered to specify certain manufacturing and other operations in relation to a class of goods that shall not be permitted in a warehouse.

ii. GST

a) Amendments for Input Tax Credit:

• The time limit for availing input tax credit for an invoice or debit note pertaining to FY 2017-18 to FY 2020-21 has been extended, allowing it to be claimed in the GST return filed by November 30, 2021.

• The restriction on input tax credit for tax paid under sections 129 and 130, as well as tax paid under section 74 for demands, has been removed for FY 2024-25 onwards. This is in lines with the substitution of section 74 by section 74A.

b) Exclusions or new exemptions:

• Extra Neutral Alcohol (ENA) used in the production of alcoholic beverages for human consumption has been excluded from the scope of GST. This will provide respite to the liquor industry as ENA is a primary ingredient in manufacture of alcohol for human consumption.

• The activity of apportioning co-insurance premiums by the lead insurer to the co-insurer shall be considered neither a supply of goods nor a supply of services, provided the lead insurer pays GST on the entire premium amount.

• The deduction of ceding commission or reinsurance commission from the reinsurance premium paid by the insurer to the reinsurer shall be shall be inserted in schedule III and considered neither a supply of goods nor a supply of services, provided the reinsurer pays the GST liability on the gross reinsurance premium.

• A new Section 11A has been introduced to empower the government to regularize any non-levy or short levy of central tax resulting from prevalent general trade practices. This is a welcome move and shall aid in reducing litigation.

c) GST Refund:

• The refund benefit for unutilized input tax credit or integrated tax has been restricted for zero-rated supplies of goods that are subject to export duty.

d) Other key amendments:

• The time of supply for services where the invoice must be issued by the recipient in reverse charge situations has been amended to insert a new sub-clause – the date of issue of self�invoices as prescribed under section 31(3)(f)

• A registered person required to deduct tax at source must file a return each month, regardless of whether any deduction has been made during that month.

• Sub-section (7) of section 140 of the CGST Act is being amended to allow for the utilization of transitional credit pertaining to eligible CENVAT credit on input services received by an Input Services Distributor before the appointed day, provided that invoices for these services were also received before the appointed date. This amendment comes into effect from 01-Jul-2017.

• A sunset clause has been prescribed for the Anti-profiteering Authority as of 31-Mar-2025. Any pending cases will be transferred to the Principal Bench of GSTAT.

iii.GST Litigation

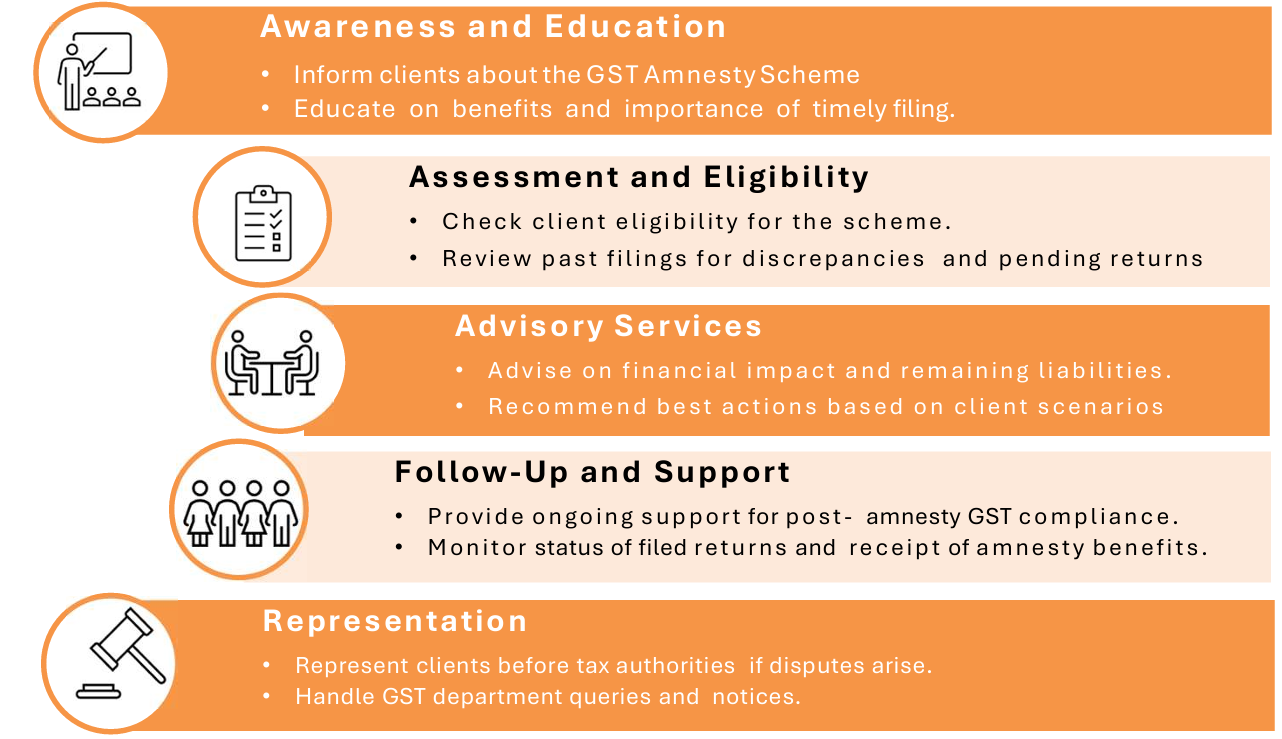

a) Conditional waiver of interest and penalty:

• Section 128A is inserted to provide a conditional waiver of interest and penalty for demand notices issued under Section 73 of the Act for the Financial Years 2017-18, 2018-19, and 2019-20 (excluding demand notices for erroneous refunds).

b) Authorized Representative can appear for summons:

Provisions have been inserted to allow an authorized representative to appear on behalf of the summoned person before the proper officer.

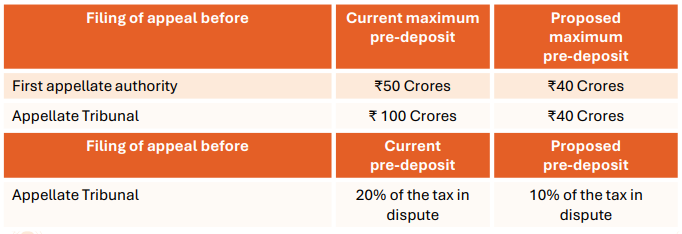

c) Reduction in the amount of pre-deposit for filing appeal:

d) Exclusive hearing before the Principal bench of Appellate Tribunal

Section 109 of the CGST Act is being amended to authorize the Government to designate specific types of cases that will be exclusively heard by the Principal Bench of the Appellate Tribunal.

e) E- Commerce Operators:

Sub-section (1B) of section 122 of the CGST Act is being amended to limit its application to electronic commerce operators obligated to collect tax at source under section 52 of the Act. This amendment will be effective from October 1, 2023, the date when the sub-section originally came into force.

SBC Comments:

The proposed amendments are designed to streamline the GST Appellate Tribunal’s operations and clarify the appeal process. They include provisions for the Government, based on the GST Council’s recommendations, to designate certain cases or categories of cases to be heard exclusively by the Principal Bench.

This is a positive development, as it ensures that industry-wide issues are addressed by the Principal Bench, following the Council’s recommendations and Government notifications.

Currently, appeals to the Appellate Tribunal must be filed within three months from the date the order is communicated. The Removal of Difficulty Order No. 09/2019-Central Tax dated December 3, 2019, clarified that the three-month period starts from the later of either the date of communication of the order or the date the President or State President of the Appellate Tribunal assumes office.

All other amendments are in line with the recommendations of the 53rd GST Council Meeting.

• The proposed amendment for ISD will provide huge relief to several taxpayers who have transitioned closing balance of erstwhile ISD directly to the GST registration which remained blocked till now.

• E-commerce operators who are required to collect tax at source under Section 52 of the CGST Act are obligated to comply with the provisions prescribed under the CGST Act.

Accordingly, the penalty provision under Section 122(1B) of the CGST Act is being amended to restrict its applicability to only to such registered E-commerce operators who are required to collect tax at source under Section 52 of CGST Act, and not in the case of other registered E-commerce operators.

• Other provisions provide the much needed certainty to the everchanging GST Laws

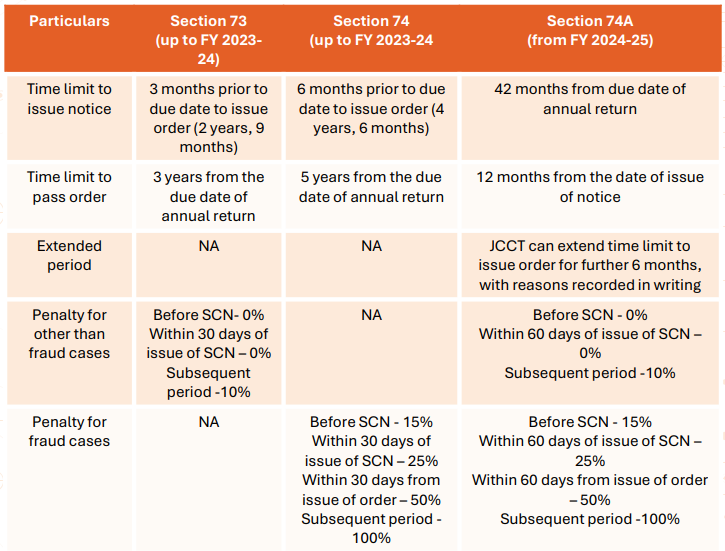

f) Harmonize the limitation period for the issuance of notices and orders for both fraud and non-fraud cases:

SBC Comments:

Section 74A is being introduced in the CGST Act to address tax liabilities related to the FY 2024-25 onwards – For tax not paid, short paid, erroneously refunded, or input tax credit wrongly availed or utilized for any reason.

Limitation period as prescribed applies irrespective of whether charges of fraud, wilful misstatement, or suppression of facts are invoked. Additionally, higher penalties are stipulated for cases involving fraud, wilful misstatement